What is a Perpetual DEX (Perp DEX)?

A perpetual DEX is an on-chain derivatives venue that lets you trade perpetual futures from a self custody wallet. You post collateral, go long or short (leverage is optional), and the position stays open until you close it or get liquidated.

Perpetuals do not expire, so the market uses funding payments to keep the perp price close to spot. Risk is enforced by smart contracts: margin requirements, liquidations, and collateral movements are rules based and auditable.

The chain you trade on affects fees, latency, and liquidation reliability. Lighter is built on Ethereum L2 infrastructure designed for low cost trading. Hyperliquid runs on its own purpose built L1. GMX runs on Arbitrum and Avalanche. Drift Protocol is built on Solana.

How Trading Fees Work on Decentralized Perps

Trading on perp DEXs has four main costs. Some are paid to the protocol (fees, liquidation penalties). Others are paid between traders (funding). Your true cost is the sum, not the headline maker fee.

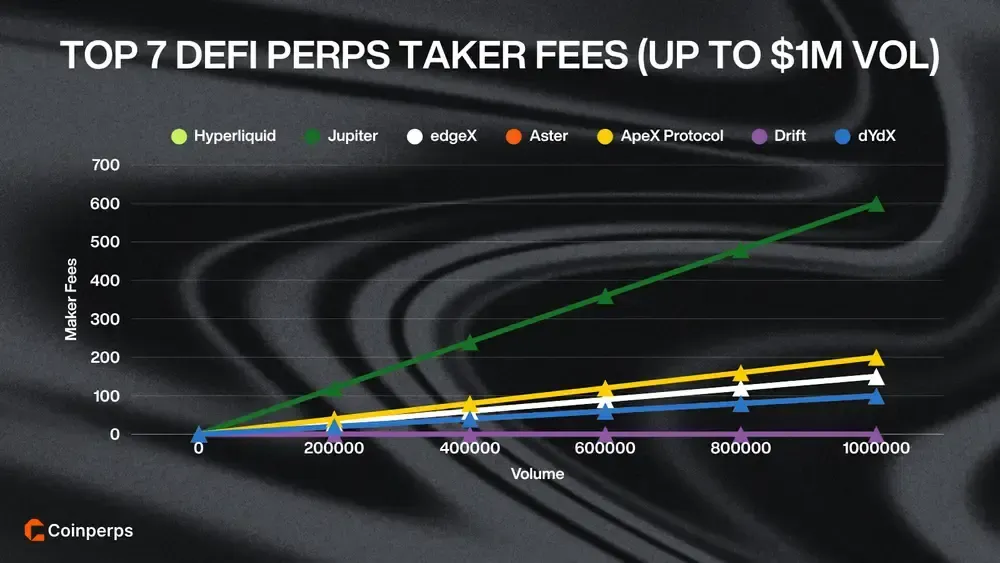

Trading fees (maker and taker)

Maker fees apply when your order adds liquidity. Taker fees apply when your order removes liquidity. Fees are usually charged on notional size when you open and close.

Not every venue follows pure maker/taker pricing. For example, Jupiter Perps charges a flat base fee on trade size for opening and closing, including limit orders.

Funding rates

Funding is a periodic payment between longs and shorts that keeps the perp price close to spot. Positive funding means longs pay shorts. Negative funding means shorts pay longs. It is not “a protocol fee” in most designs, it’s a transfer between traders.

Liquidation fees and penalties

Liquidation happens when collateral drops below maintenance requirements. The close is forced, and the fill includes a penalty or fee set by the market, which is why liquidation is usually worse than “just closing manually.”

Network fees

Some perp DEXs require chain gas for actions like deposits, approvals, and trading. Others abstract gas away and charge only trading fees.

On GMX, trading settles on Arbitrum, so you generally pay Arbitrum gas for on-chain actions. In normal conditions, Arbitrum transactions are often around the ten-cent range, but it varies with congestion and action type.

Hyperliquid does not charge gas for placing or canceling orders, but it does have a one-time activation fee mechanic for new accounts.

Risks When Using DeFi Perpetual Exchanges

Our engine continuously aggregates trading data across BTC, ETH, and major altcoin perps, standardizing every metric to ensure fair comparisons between centralized and decentralized exchanges.

- Liquidity & Market Depth (35%) - Order book depth, open interest, 24-hour volume, and average slippage measured directly from live exchange data.

- Fees & Funding (25%) - Maker/taker fees, funding rate consistency, and rebate structures verified through API endpoints.

- Execution & Stability (20%) - Latency, uptime, and liquidation system performance derived from real-time platform data.

- Security & Compliance (20%) - Licensing, proof-of-reserves transparency, and historical security record where available.

CoinPerps rankings update every 10 seconds, capturing live shifts in liquidity, pricing, and execution conditions across the perpetual market. For more information, read our full methodology.

How Trading Fees Work on Perpetual Exchanges

DeFi perpetual exchanges can be fast and capital efficient, but the risk stack is different from a centralized venue. The biggest risks come from contract code, liquidation mechanics, thin liquidity, and how prices are sourced on-chain.

- Smart contract vulnerabilities: A single bug can drain collateral or break accounting. GMX V1 was hit for roughly $42 millionin July 2025 through a reentrancy path in the vault and order flow logic, with funds later returned after a bounty arrangement.

- Liquidation risk: Perps are leveraged by design, so small spot moves can wipe margin. Liquidations are forced closes, often during volatility, and the fill can be worse than a manual exit when order books thin out or blocks get congested.

- Liquidity and slippage risk: On-chain liquidity can disappear quickly, especially in smaller markets. Large orders move price when there is not enough depth, leading to slippage and poor entry or exit pricing.

- Oracle and price manipulation: Perps are only as safe as their price feed. Flash loans and TWAP manipulation can skew oracle prices, leading to inaccurate liquidations and incorrect collateral valuation.

- MEV, front-running, and sandwiching: Front-running and sandwiching can materially worsen execution. Ethereum has been reported to see over 10,000 unfair trades per day, with user losses exceeding $14 billion per month, according to EigenPhi.

- Governance and upgrade key risk: Many perp DEXs can still be changed by privileged roles. Admin keys, multisigs, and upgrade paths can introduce real trust assumptions, especially if there is no timelock or clear emergency process.

- Cross-chain and bridge risk: Multi-chain perps add bridge and messaging risk on top of trading risk. Aster operating across Arbitrum and BNB Chain is an example where bridging complexity increases the attack surface.

- Recovery and insurance limitations: Post-hack recovery is uncommon and rarely guaranteed. Even when partial returns occur, as in GMX’s recovery, the cost can be borne by liquidity providers or the protocol treasury rather than being made whole by insurance.

Perp DEX risk is mostly about market structure and code, not the token’s price trend. You can still get wrecked by thin liquidity, oracle issues, chain congestion, or liquidation mechanics even if your trade direction is right.