Perpetual Exchange Regulation Explained: DEX & CEX

Find out where crypto perpetual trading is legal, restricted, or tightly licensed in 2026, with clear coverage of DEX, CEX, and tax rules for different countries.

Fact checked

Key Takeaways:

- Crypto perpetual regulations are tightening unevenly, with the US, EU, HK, and Australia building clearer pathways while the UK, Canada, and much of Africa are stricter.

- CEX perps fit more easily into licensing, disclosure, and surveillance regimes, while DEXs face murkier treatment focused on interfaces, access points, promotion, and enforcement.

- Tax treatment usually follows derivatives, capital-gains, or income-tax rules, with reporting expanding as DAC8, CARF, and broker-reporting frameworks move into force.

Crypto perpetual regulation is becoming more structured in 2026, but the pace still differs by region, user type, and product design. Some markets are opening regulated access, while others are tightening retail limits, licensing standards, reporting rules, and enforcement.

That makes a side-by-side summary useful for readers who want the practical picture quickly. The table below condenses regional outlooks, CEX-versus-DEX treatment, and tax direction into an easier snapshot than long-form legal analysis alone.

Quick global snapshot of regulation, structure, and taxation:

Perpetual Exchange Regulation in the USA

In the U.S., crypto perpetuals sit mainly under the CFTC and the Commodity Exchange Act, with Dodd-Frank shaping swaps oversight and the NFA supervising intermediaries. The SEC still matters where token status, broker-dealer activity, or securities-based products are implicated.

The biggest recent shift is onshore product expansion. Coinbase began offering CFTC-regulated nano Bitcoin and Ether perpetual futures in July 2025, while Cboe launched Bitcoin and Ether Continuous Futures in December 2025, giving U.S. traders a regulated perpetual-style alternative.

As of March 2026, exchanges currently or recently allowed to offer crypto perpetual or perpetual-style exposure include Coinbase Derivatives, Cboe Futures Exchange, CME Group, Kraken Derivatives US, and Robinhood’s regulated futures stack, though product scope differs and not every venue lists true perps.

The near-term outlook is more coordination, not less. On March 11, 2026, the SEC and CFTC signed a fresh cooperation MOU, while new CFTC filings suggest additional onshore perp-style listings, so 2026 likely brings more regulated leverage and tighter market-surveillance expectations.

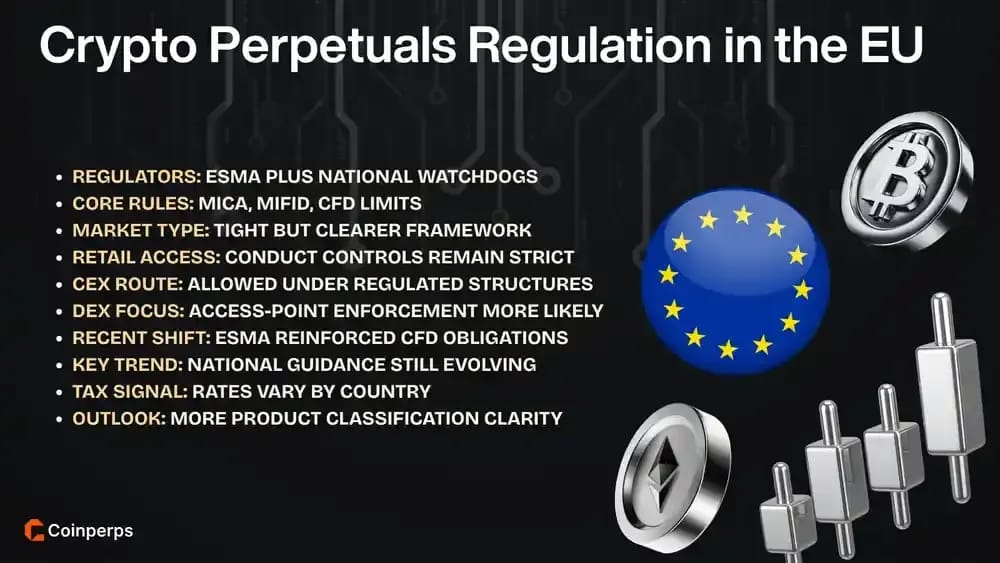

How Are Crypto Perpetuals Regulated in the EU?

In the EU, crypto perpetuals are increasingly treated through MiCA, MiFID II, national CFD restrictions, and product-governance rules rather than a single perp-specific statute.

Key regulatory milestones across the bloc:

- MiCA framework: MiCA created the EU’s core crypto rulebook, but derivatives still mostly fall through MiFID II and national investment-services regimes.

- CFD intervention legacy: ESMA’s long-running CFD intervention is still highly relevant because many leveraged “perpetual futures” can still be classified as CFDs.

- February 2026 warning: ESMA said firms must assess whether crypto perpetuals fall inside CFD measures and comply with investor-protection obligations.

- MiFID compliance burden: Where a perp is treated as a financial instrument, firms face appropriateness testing, product governance, conflicts controls, and PRIIPs requirements.

- Retail-access reality: EU access is improving, but leverage-heavy products are filtered through national conduct rules, marketing restrictions, and suitability expectations.

- March 2026 market development: Coinbase started rolling out regulated futures in 26 European countries through its MiFID-regulated European entity.

- Likely next phase: Expect more national guidance in 2026 clarifying whether specific perpetual structures are CFDs, futures, or prohibited retail products.

Crypto Perpetual Regulations in the United Kingdom

The UK is one of the strictest major markets for retail crypto derivatives. Under FCA rules, the retail marketing, distribution, and sale of cryptoasset derivatives are prohibited, even as the broader UK crypto regime moves into formal FSMA-based rulemaking.

That means retail traders still cannot lawfully access crypto perpetuals from FCA-authorized firms, although the FCA separately reopened retail access to crypto ETNs in 2025. The regulator has made clear that the derivatives ban stays in place despite wider market reforms.

The direction of travel is clearer than the immediate result. New UK cryptoasset regulations were published in early 2026, the FCA opened further consultations in January 2026, and firms can apply from September 30, 2026, ahead of the planned October 25, 2027 regime start.

Perpetual Exchange Regulation in Canada

Canada regulates crypto perpetual exposure primarily through provincial securities law, CSA oversight, and CIRO membership rules rather than a bespoke national perp statute. In practice, platforms offering crypto contracts are often treated as dealing in securities or derivatives.

The regulatory mood is cautious. In 2024, CSA and CIRO told crypto trading platforms to prioritize investment-dealer registration and CIRO membership, and in February 2026 CIRO added new digital-asset custody guidance that tightens operational expectations for registered platforms.

So Canada is not a permissive retail-perps market. The near-term path is more compliance, custody, and dealer-registration work, not a sudden opening for offshore-style leveraged perpetuals, though authorized crypto platforms and funds continue gaining clearer rulebooks.

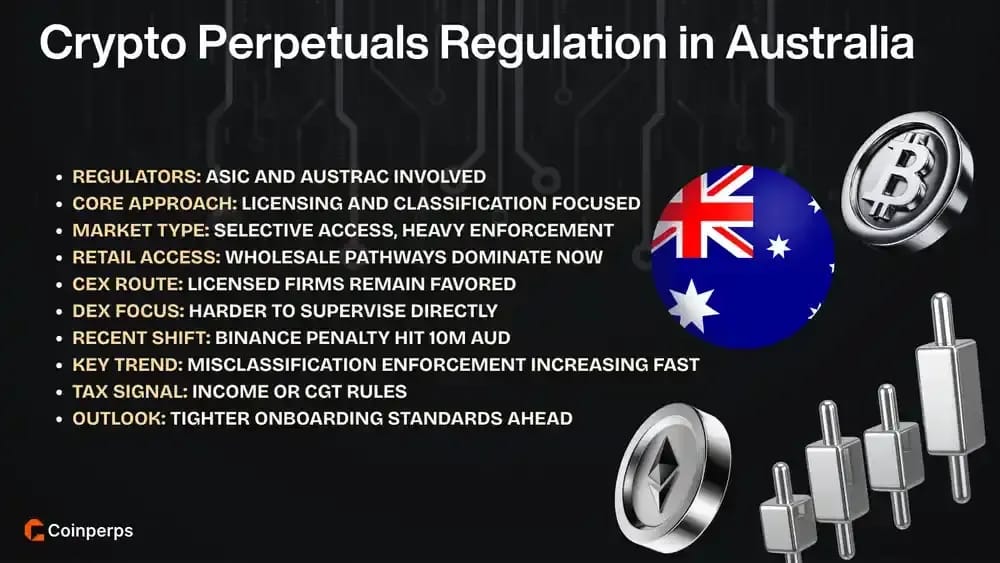

Crypto Perpetuals Regulations in Australia

Australia treats crypto perpetuals as financial products, so exchange operators and intermediaries face licensing, design-and-distribution, and client-classification rules enforced mainly by ASIC.

Major milestones and enforcement signals:

- Wholesale-client gatekeeping: Australian crypto derivatives are generally limited to wholesale clients unless firms can satisfy stricter retail-product obligations.

- Binance licence retreat: Binance Australia Derivatives lost its Australian financial services licence in 2023 after regulatory scrutiny intensified.

- Kraken compliance pressure: ASIC sued Bit Trade over Kraken’s margin product, arguing the offering triggered financial-product and design-distribution obligations.

- March 2026 penalty: On March 27, 2026, Binance Australia Derivatives was ordered to pay 10 million AUD for onboarding failures.

- Consumer-protection focus: ASIC said more than 85% of Binance Australia Derivatives clients were wrongly classified, causing over 12 million AUD in losses and fees.

- Current market shape: Regulated access still exists, but mainly for wholesale users through firms able to meet licensing, onboarding, and suitability standards.

- Near-term outlook: Expect sharper enforcement on misclassification, disclosure, target-market determinations, and leverage controls rather than a lighter-touch rulebook.

Perpetual Exchange Regulation in Asia

Asia has no single model: Japan and Singapore lean institutional, Hong Kong is opening carefully, while other markets still restrict retail leverage or keep perps offshore.

Country-by-country snapshot across major Asian markets:

- Hong Kong: The SFC published frameworks in February 2026 allowing licensed VATPs to offer perpetual contracts to professional investors only.

- Singapore: MAS stands as conservative on retail crypto risk, but SGX launched institutional-grade Bitcoin and Ether perpetual futures infrastructure.

- Japan: The FSA is pushing crypto toward the Financial Instruments and Exchange Act, which would tighten market-abuse and investor-protection rules.

- South Korea: Domestic spot liberalization is progressing for institutions, but retail offshore-style crypto perpetuals are heavily constrained.

- India: Crypto is heavily taxed and fragmented domestically, while regulated derivatives innovation is more plausible in GIFT City than onshore retail platform.

- Philippines: The SEC’s 2025 CASP rules formalized licensing for crypto service providers, but that does not equal a broad retail-perpetual green light.

- UAE/Dubai: VARA has become one of the clearest licensing routes for virtual-asset firms, including derivative ambitions.

How Are Crypto Perpetuals Regulated in Americas?

Outside the U.S. and Canada, the rest of the Americas is split between cautious Mexico, fast-moving Cenral American rulemaking, and still-fragmented South American supervision.

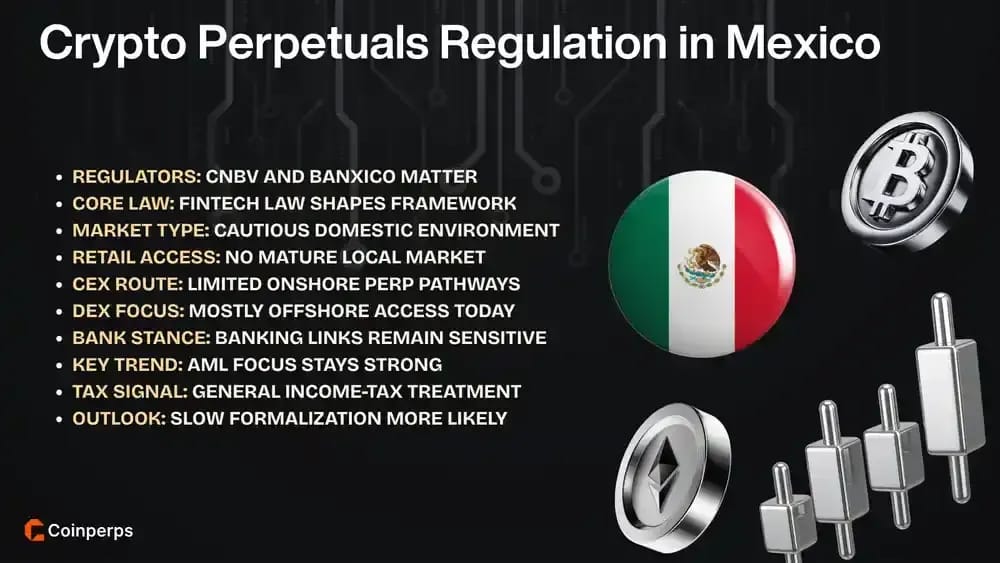

Mexico

Mexico still takes a conservative line. The core framework comes from the Fintech Law, CNBV supervision, and Banco de México’s power over authorized virtual-asset use inside regulated institutions, which helps explain why most perpetual offerings are offshore.

So while crypto itself is not banned, onshore regulated retail crypto perps are not a developed domestic category. The practical risk is marketing, licensing, and AML exposure rather than a well-defined local pathway for leveraged perpetual exchanges.

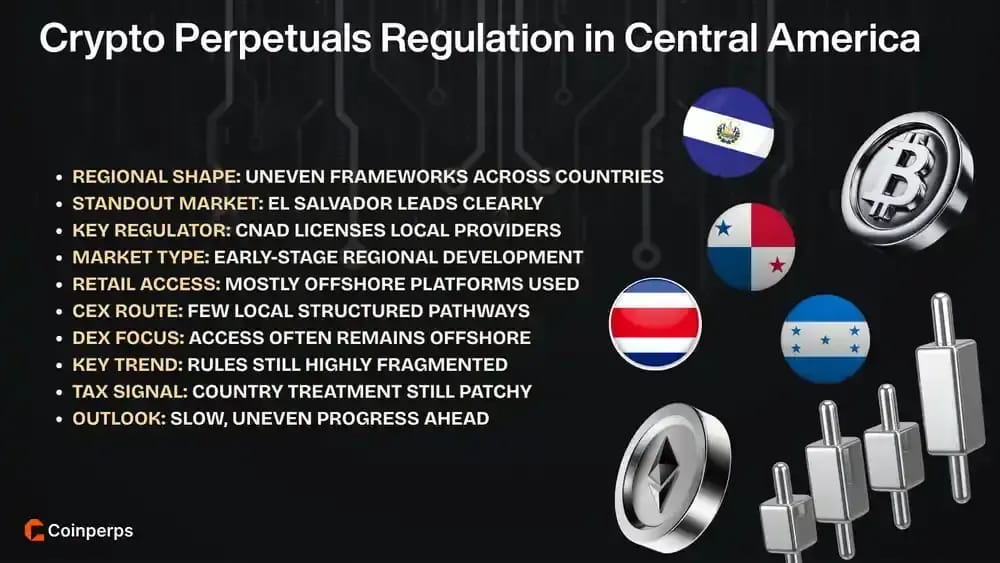

Central America

Central America does not yet have a single, mature onshore market for retail crypto perpetuals. Instead, the region ranges from El Salvador’s dedicated digital-asset regime to countries where crypto is legal but mostly unlicensed, lightly defined, or restricted inside the banking system.

Main regulatory patterns across Central America:

- El Salvador: The clearest regional framework, with CNAD supervising the digital-asset ecosystem and licensing digital-asset service providers under the country’s dedicated regime.

- Panama: Still lacks a fully enacted, bespoke crypto licensing law, so exchange activity mainly depends on existing AML and corporate-law compliance.

- Costa Rica: Crypto is not prohibited, but firms still work through general tax, AML, and business-law analysis rather than a dedicated perp rulebook.

- Guatemala: No specific crypto law is in force yet, so digital-asset use is mostly tolerated under private-law logic rather than actively licensed.

- Honduras: The Central Bank has warned that crypto lacks legal backing, while regulated financial institutions face stricter limits on crypto dealings.

- Regional takeaway: For now, compliant perpetual offerings in Central America are far more likely to sit offshore than inside a fully local derivatives framework.

South America

South America is more progressive on crypto adoption than on perpetual-specific law, with each country using existing market, tax, and consumer-protection tools first.

Main patterns across the subregion:

- Brazil leads on structure: Brazil is the region’s most institutionally developed market, with B3 expanding digital-asset ambitions into 2026.

- Andean markets is cautious: Peru, Ecuador, and Bolivia remain more restrictive or underdeveloped for compliant leveraged crypto products.

- Tax visibility is rising: Brazil, Chile, Argentina, and Colombia are among jurisdictions committed to CARF-style reporting implementation timelines.

- Policy trend: Expect more AML, disclosure, and reporting rules before broad retail authorization for domestic crypto perpetual platforms.

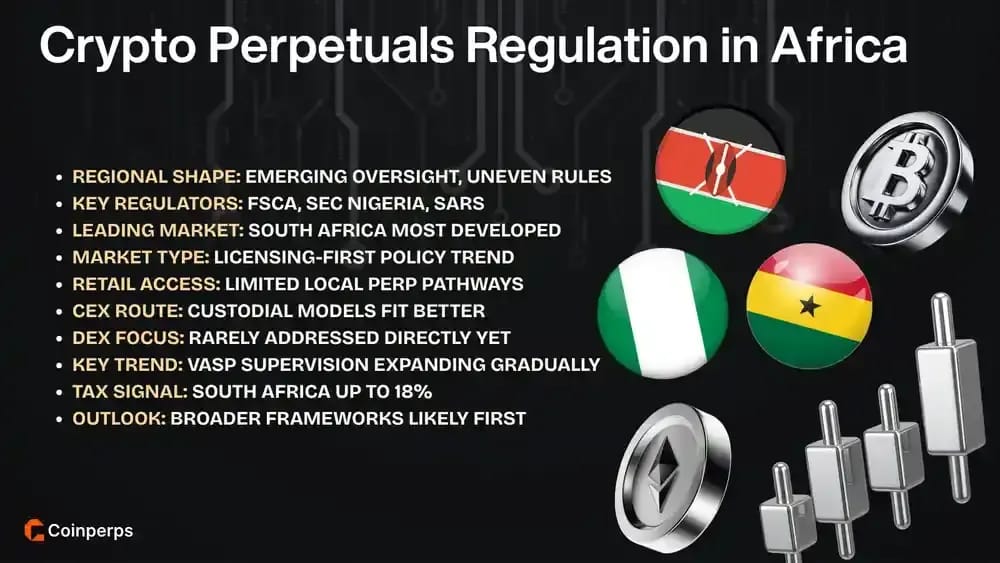

Are Perpetual Exchanges Regulated in Africa?

Africa is moving from patchwork tolerance to formal supervision, but perpetual exchanges are still rarely addressed head-on. Most countries focus first on licensing VASPs, AML, consumer protection, and whether crypto qualifies as a financial product or security.

South Africa is the continent’s clearest example of formal market supervision: the FSCA has licensed hundreds of crypto-asset service providers under FAIS. Mauritius also offers a structured VAITOS regime, while Nigeria’s 2025 ISA gave the SEC clearer digital-asset authority.

Kenya is the newest major mover. Its 2025 VASP Act is now being operationalized through draft 2026 regulations, while countries such as Ghana, Rwanda, and others are still earlier-stage. So yes, regulation exists, but compliant onshore crypto perps are limited.

Differences Between CEX and DEX Perpetual Regulations

Across all major regions, CEX perpetuals are easier for regulators to police, while DEX perpetuals create harder questions around intermediaries, interfaces, and jurisdiction.

How the split looks by region:

- USA: CEX perps can fit inside CFTC-supervised futures rails; DEX perps trigger harder questions around front ends, wallet interfaces, and intermediating activity.

- EU: CEXs face MiFID, CFD, and product-governance rules; DEX offerings are harder to police directly, so regulators focus on firms, marketing, and access points.

- UK: FCA-authorized CEXs cannot market crypto derivatives to retail users; DEX use may still occur offshore, but UK-facing promotion are the pressure point.

- Canada: CEXs are pulled into dealer-registration and CIRO membership; DEX models avoid some formality but raise even sharper enforcement and investor-protection concerns.

- Australia: CEX oversight centers on licensing and client classification; DEX access is harder to ringfence, so enforcement often targets onboarding and local solicitation.

- Asia: Hong Kong and Singapore can license institutional CEX products; DEX perpetuals are far less compatible with local conduct and surveillance expectations.

- Mexico and Latin America: CEXs are the visible compliance target for AML, tax, and marketing rules; DEXs are operationally accessible but legally murkier.

- Africa: Where licensing exists, it mainly fits CEX or custodial models; DEX perpetuals usually sit outside the first wave of local rulebooks.

How Are Crypto Perpetuals Taxed Around the World?

Crypto perpetuals are usually taxed under broader rules for derivatives, trading income, capital gains, and exchange reporting, so outcomes depend on product structure, trader activity, and each jurisdiction’s disclosure regime.

United States

In the United States, crypto perpetual tax treatment depends first on venue and contract design. Regulated futures can fall under Section 1256, which applies mark-to-market accounting and the favorable 60/40 long-term and short-term capital-gains split.

Offshore or unregulated perpetuals are generally taxed under ordinary digital-asset rules instead, meaning gains or losses are reported transaction by transaction. Reporting pressure is also rising as the IRS expands digital-asset broker compliance and information-reporting expectations.

European Union

Across the European Union, there is still no single tax rate for crypto perpetuals. Member states decide whether profits are treated as capital gains, miscellaneous income, or business income, depending on holding period, scale, and legal structure.

Country differences is sharp. Germany still allows tax-free treatment for certain private crypto disposals after a one-year holding period, while DAC8 has standardized reporting timelines across the bloc, with the new crypto transparency rules applying from January 1, 2026.

United Kingdom

In the United Kingdom, crypto perpetual profits are usually taxed under ordinary capital-gains or income-tax principles, depending on whether the activity looks more like investment or trading. HMRC’s Cryptoassets Manual is the main interpretive guide for taxpayers.

For most chargeable assets, current UK capital-gains tax rates are 18% for gains within the basic-rate band and 24% for higher-rate taxpayers. Separately, CARF reporting preparation began from January 1, 2026, increasing expected transparency between platforms and HMRC.

Canada

Canada generally taxes crypto profits either as capital gains or as business income, with the distinction turning on frequency, commercial intent, sophistication, and overall behavior. CRA guidance is principles-based rather than creating a separate, perpetual-specific tax category.

That classification matters because only half of a capital gain is included in taxable income, while business income is fully taxable. As reporting frameworks spread internationally, Canadian crypto traders should expect steadily greater visibility around offshore and platform-based activity.

Asia-Pacific

Asia-Pacific combines very different tax models. Japan generally taxes crypto under miscellaneous income rules, which can reach high progressive rates, while other markets focus more on exchange reporting and classification than on creating perpetual-specific tax treatment.

Japan is the clearest example of high-rate treatment, with crypto income commonly described as reaching an effective 55% ceiling under progressive taxation. Meanwhile, more Asia-Pacific jurisdictions are preparing CARF implementation timelines that will increase cross-border tax reporting from 2027 onward.

Central and South America, plus Africa

Outside North America, the main theme is reporting consistency rather than rate uniformity. Countries across Central America, South America, and Africa are moving toward CARF-style exchange commitments, even where local crypto-derivatives taxation still relies on older income-tax and gains-tax principles.

Examples already show the range. South Africa applies normal income-tax principles to crypto and may tax gains on either revenue or capital account, while OECD commitment tables now include countries such as Brazil, Chile, Colombia, Mauritius, Mexico, Panama, and Rwanda.

Bottom Line

In 2026 crypto perpetuals sit inside a patchwork of national rules built around selective access, retail protection, and increasingly strict licensing demands.

The clearest pattern is that centralized exchanges can win permission by fitting inside existing futures, securities, or investment-services frameworks. Decentralized perpetual protocols are harder to supervise and therefore face more fragmented, interface-focused enforcement pressure.

For traders and exchanges alike, the practical takeaway is simple: access is expanding, but only where firms accept heavier licensing, reporting, tax, and investor-protection obligations. In 2026, compliance is becoming the real listing standard.

Frequently asked questions