Crypto Perpetual Futures Regulation Explained

Discover how global crypto perpetual futures regulation is unified by mandatory KYC, strict geo-blocking, and enforcement targeting offshore providers.

Fact checked

Key Takeaways:

- North America and Europe established strict jurisdictional authority, enforcing mandatory exchange registration for crypto perpetual futures regulation.

- Smaller markets like Australia's 2x limit and Singapore's ban confirm a swift, decisive global trend toward high-compliance, restrictive trading environments.

- The CFTC's Ooki DAO case affirmed that decentralized protocols face contributor liability, forcing them to adopt strict geo-blocking measures against retail users.

The global crypto derivative market, valued in the trillions, faces an escalating regulatory challenge as high-leverage perpetual futures contracts pose considerable systemic and consumer risks. Jurisdictions are struggling to fit these unique instruments into existing financial laws.

The key nuance lies in regional divergence: North America pursues enforcement-led prohibition, while Europe and Asia focus on licensing regimes that impose low leverage caps, driving volume to non-compliant offshore platforms.

Continue reading to map crypto perpetual futures regulation. ⬇️

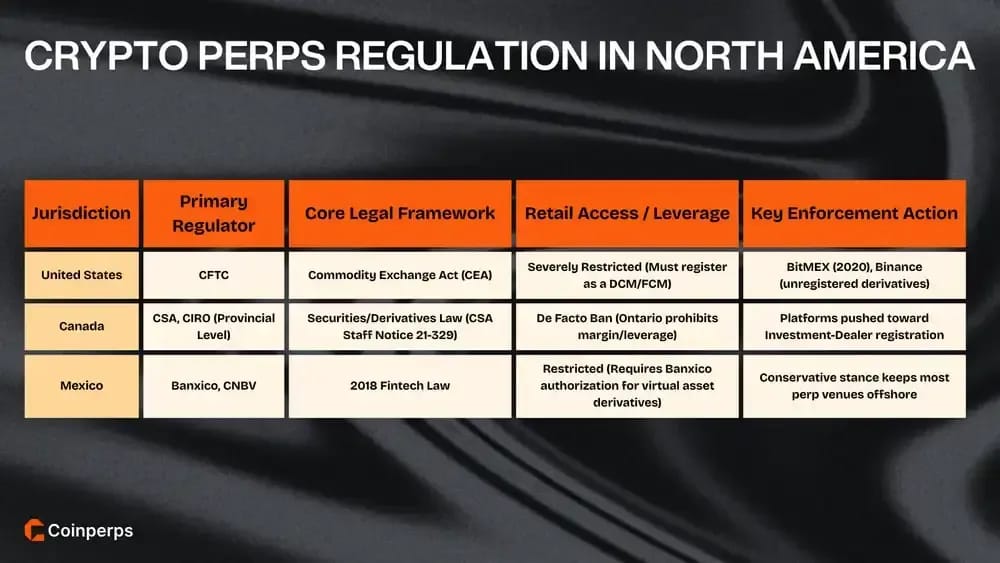

Crypto Perpetual Futures Regulation in North America

North America regulates crypto perpetual futures mainly through existing derivatives, securities, and AML frameworks rather than crypto-specific “perps” statutes.

The key compliance question is which agency has jurisdiction over the product and whether the platform’s access controls, registrations, and supervision match that classification.

1. United States

The Commodity Futures Trading Commission (CFTC) has exclusive jurisdiction over cryptocurrency derivatives in the US, classifying Bitcoin and Ether as commodities under the Commodity Exchange Act. Any platform selling futures to US residents must register as a Designated Contract Market.

Retail access to perpetuals is severely restricted, with most offshore platforms blocking US IP addresses to avoid enforcement actions. The regulatory framework prioritizes institutional clearing and strictly enforced Know Your Customer (KYC) protocols, preventing unregistered exchanges from servicing Americans.

Q4 2025 marked a shift: a joint SEC/CFTC statement and a CFTC pilot program enabled regulated Designated Contract Markets, including Coinbase Derivatives, to compliantly launch Bitcoin, Ether, and USDC perpetual-style futures, ensuring legitimate access.

2. Canada

Canada routes perpetual-like exposure through securities-and-derivatives law at the provincial level. Joint CSA/IIROC Staff Notice 21-329 (29 March 2021) treated many “crypto contracts” as securities or derivatives, pushing platforms toward dealer registration and CIRO-style supervision.

Ontario’s securities regulator explicitly prohibits registered platforms from offering margin or leverage to retail clients, effectively banning perpetual futures for the average user. Platforms operating under the pre-registration undertaking must segregate client assets and avoid offering proprietary leverage products.

By August 2024, CSA and CIRO told CTPs facilitating crypto-based securities/derivatives to prioritize investment-dealer registration and CIRO membership. CIRO’s February 2025 bulletin repeats that framing and points applicants to dealer-member checklists, webcasts, and practical tooling.

3. Mexico

Mexico’s 2018 Fintech Law recognizes “virtual assets,” but channels most activity through regulated financial entities and Banco de México. For perp-style products, the key constraint is that derivative instruments with underlying virtual assets require Banxico-set conditions and authorizations.

Banxico’s fintech regulations explicitly say FTIs may only participate in operating, designing, or commercializing derivatives on virtual assets subject to Banxico’s requirements and prior authorizations; so an exchange can’t assume “derivatives are unregulated” just because spot trading exists.

CMS’s 2025 Mexico guide describes a conservative stance on virtual assets by Mexican regulators, with CNBV supervising institutions and Banxico issuing the operative rules. That reality explains why many perp venues stay offshore while marketing remains a compliance tripwire.

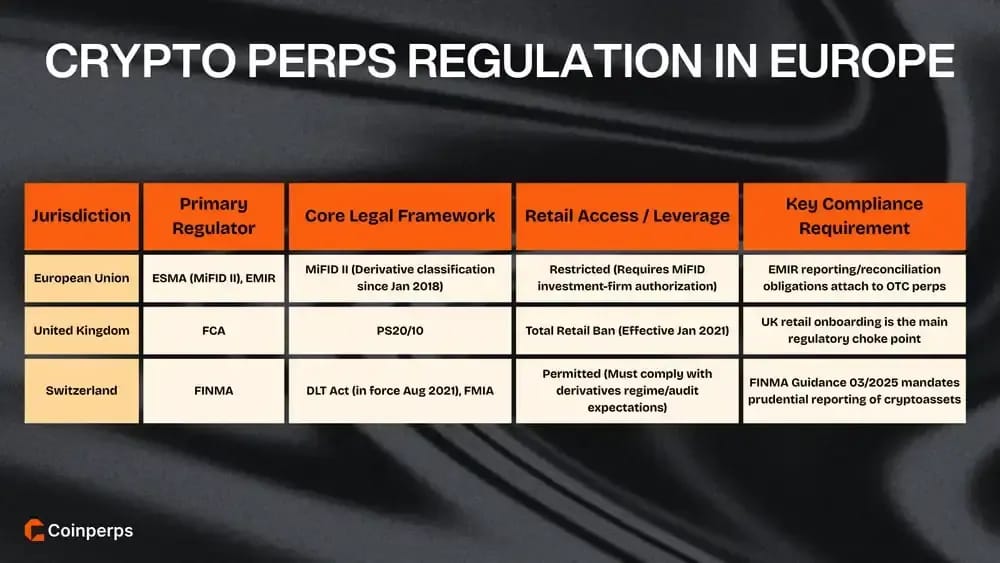

Crypto Perpetual Futures Regulation in Europe

Europe approaches perpetual futures through mature financial-instruments rules, with derivatives classification often determining whether MiFID II, EMIR, or domestic restrictions apply.

The practical outcome is that venue authorization, retail distribution limits, and reporting duties typically matter more than the contract’s on-chain mechanics.

1. European Union (EU/EEA)

In the EU/EEA, perpetual futures are regulated as derivatives under MiFID II’s financial-instruments perimeter (Directive 2014/65/EU), applied from 3 January 2018. That pulls venues toward investment-firm authorization, conduct rules, and product governance instead of “crypto-only” regimes.

MiCA’s 2024-2025 go-live dates didn’t “capture perps”; ESMA’s 2024 final report stresses that when something qualifies as a MiFID II financial instrument, MiFID II applies rather than MiCA. Perps marketing often hinges on this classification line.

For OTC-style perps offered bilaterally, EMIR (Regulation 648/2012) matters: it’s the EU’s framework for OTC derivatives, CCPs, and trade repositories. Reporting, reconciliation, and portfolio risk-mitigation expectations can attach even when the underlying is a cryptoasset.

2. United Kingdom

The UK chose a blunt retail perimeter: the FCA banned the sale, marketing and distribution of crypto-derivatives and crypto-ETNs to retail consumers, effective 6 January 2021. The ban explicitly covers CFDs, options and futures referencing certain cryptoassets.

Publication PS20/10 frames the FCA’s case as valuation, volatility and market-abuse risk that ordinary disclosure can’t fix. For perp venues, that means UK retail onboarding is the main regulatory choke point, not whether the contract is a ‘future’ on-chain.

The FCA’s own warning is operational: any firm offering these products to UK retail is ‘likely to be a scam’. That language has driven aggressive perimeter messaging and makes affiliate marketing and introducer arrangements unusually risky.

3. Switzerland

Switzerland didn’t write “perpetual futures” rules; it extended existing financial-market law via the DLT Act, fully in force from 1 August 2021. That act amended multiple federal statutes and enables regulated trading infrastructures for tokenised instruments.

On derivatives specifically, Swiss authorities have assessed whether the existing derivatives regulatory regime under the FMIA can apply to DLT-based derivatives, concluding the framework is generally adaptable. For perp issuers, that points to familiar obligations, not a blank slate.

FINMA’s 2025 Guidance 03/2025 illustrates the supervisory style: it drills into disclosure and reporting of ‘cryptobased assets’ in prudential reporting after the DLT Act. Perp businesses tied to regulated entities inherit these back-office, audit, and reconciliation expectations.

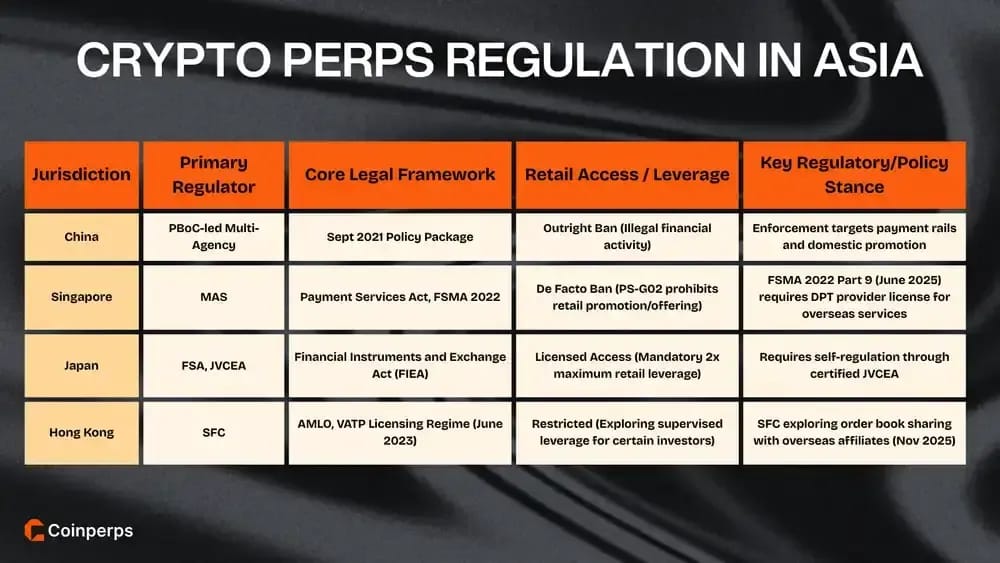

Crypto Perpetual Futures Regulation in Asia

Asia is highly fragmented on perpetual futures, ranging from outright bans to tightly licensed market access with strict promotion and investor-protection rules.

Because many regimes focus on who is solicited and where services are “provided,” cross-border structuring and marketing controls often become the main enforcement surface.

1. China

Mainland China treats crypto perps as an illegal financial activity. The PBoC-led September 2021 notice targets ‘virtual currency trading and speculation’ and anchors enforcement in multiple laws, with local governments coordinating policing, telecoms and cyber authorities.

The same 2021 policy package is commonly cited for prohibiting crypto-related financial services, including derivatives-style transactions. That means a perp venue serving mainland residents faces not just licensing issues, but allegations of operating an illegal futures business.

Because the framework is prohibition-based, compliance talk shifts to exposure: payment rails, marketing channels, and employee presence in China become the enforcement surface. Even ‘offshore’ matching engines can be swept in when promotion or onboarding touches domestic systems.

2. Singapore

Singapore splits DPT services from derivatives regulation. The Payment Services Act 2019 licenses DPT service providers, while derivative contracts are handled via the securities-and-futures perimeter. MAS’s PS-G02 guidelines also reference ‘payment token derivatives’ when describing conduct expectations.

MAS’s PS-G02 guidelines (17 Jan 2022) discourage mass-market promotion of DPT services and explicitly say DPT providers should not promote or offer payment token derivatives to the public. For perp businesses, that targets influencer marketing, ATMs, and retail funnels.

From 30 June 2025, Part 9 of Singapore’s FSMA 2022 licenses Digital Token Service Providers, even when they serve overseas customers from Singapore. MAS said it will rarely issue licences, forcing perp desks to close, relocate, or restructure.

3. Japan

Japan brought crypto-asset derivatives into a statutory perimeter in May 2020, via amendments to the Payment Services Act and the Financial Instruments and Exchange Act. FSA materials describe crypto-asset derivative transactions as regulated under the FIEA for investor protection.

Retail leverage is not a market choice in Japan. Industry materials widely cite a 2x maximum leverage for individuals on crypto derivatives, reflecting a clear policy preference for reducing liquidation spirals typical in perpetual futures.

Japan also relies on certified self-regulation. JVCEA states it is a self-regulatory organization for crypto-asset exchange services and related derivative transactions, recognized under the Payment Services Act and the Financial Instruments and Exchange Act, officially.

4. Hong Kong

Hong Kong’s VATP regime started 1 June 2023 under the AMLO framework, with SFC guidelines and a licensing handbook for platform operators. Briefings note pre-existing platforms had to apply by 29 Feb 2024 or exit by 31 May 2024.

In February 2025, Reuters quoted the SFC saying Hong Kong was exploring approval of crypto derivatives and margin lending for certain investors. The signal matters: regulators are moving from spot-only licensing toward supervised leverage, rather than pushing perps offshore.

Liquidity policy shifted again in November 2025. Reuters reported the SFC would let licensed VATPs share order books with overseas affiliates, reversing a Hong Kong-only constraint. For perp-style markets, that’s a change to matching, surveillance, and market integrity design.

5. Other Asian Markets

Across the broader Asian continent, diverse regulatory frameworks have emerged, ranging from strict licensing regimes to complete prohibitions on high-risk derivatives.

Key regulatory stances in other major Asian markets include:

- South Korea: Regulators (FSC) strictly prohibit domestic issuance of crypto futures, forcing local investors to access high-leverage products through offshore international exchanges.

- India: High taxation disincentivizes trading, while the FIU blocks access to offshore platforms lacking local anti-money laundering registration and compliance.

- Indonesia: Regulatory oversight recently transferred to the OJK, maintaining a permitted but tightly supervised environment for crypto derivative trading products.

- Thailand: The SEC Thailand bans the use of crypto for payments while maintaining a restrictive licensing regime for digital asset futures.

- Taiwan: The Financial Supervisory Commission currently classifies crypto as virtual commodities, preparing a special law to strictly regulate derivative offerings.

- Vietnam: A 2025 pilot program aims to legalize and monitor digital asset exchanges, moving away from previous legal ambiguity regarding trading.

- Malaysia: The Securities Commission permits derivatives trading only on registered Digital Asset Exchanges complying with strict recognised market operator guidelines.

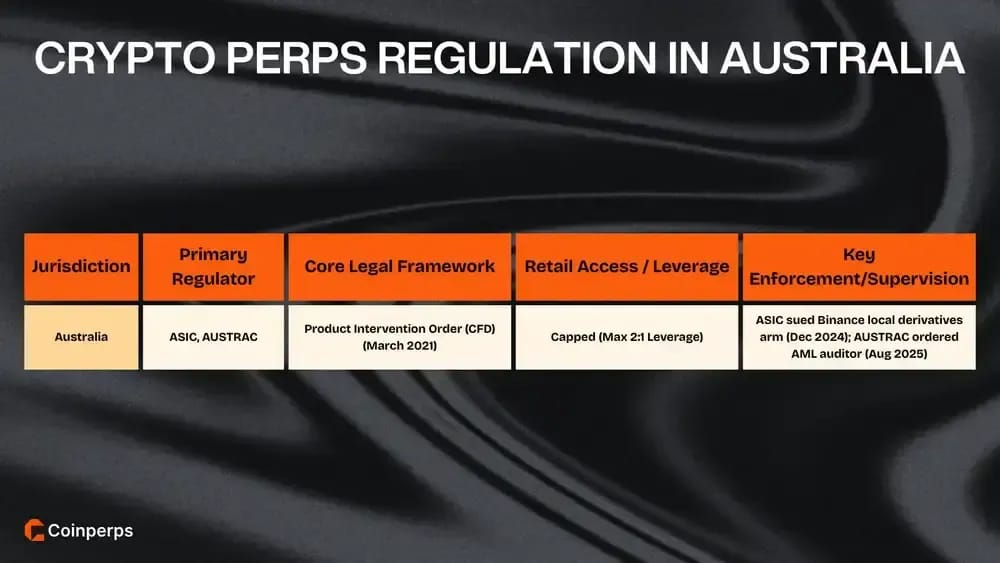

Crypto Perpetual Futures Regulation in Australia

Australia often captures retail ‘perps’ via the CFD channel. ASIC’s product intervention order took effect 29 March 2021 and capped leverage for CFDs referencing crypto-assets at 2:1, alongside margin close-out and negative-balance protections that reshape perp-like risk.

ASIC has enforced those conduct expectations against crypto-derivatives firms. In December 2024, Reuters reported ASIC sued Binance’s local derivatives arm, after cancelling its licence in April 2023 and overseeing compensation for retail clients misclassified as wholesale.

Regulators have also targeted crypto-derivatives controls through AML supervision. In August 2025, Reuters reported AUSTRAC ordered Binance’s Australian unit to appoint an external auditor after reviewing AML/CTF weaknesses, an operational test that hits perp platforms hard.

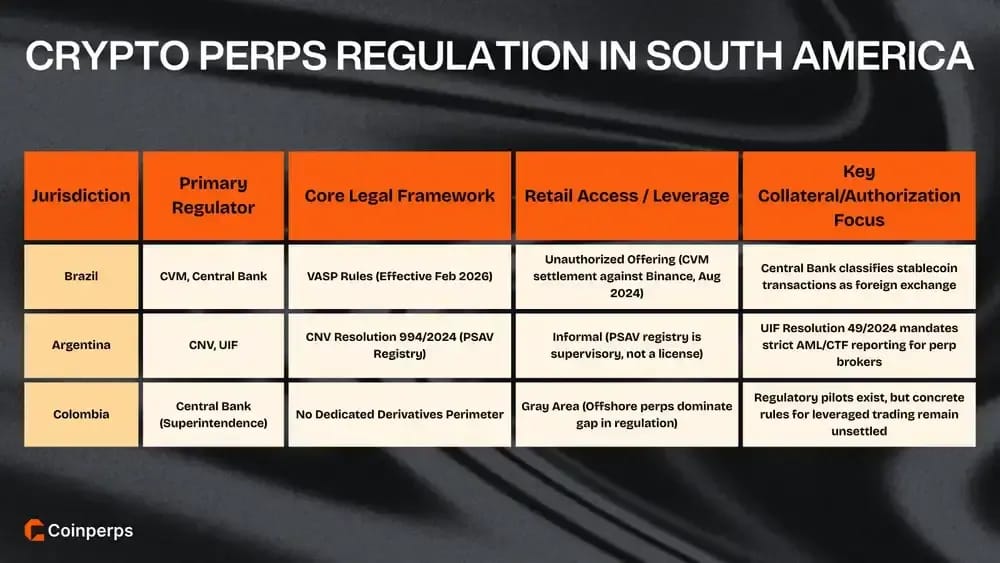

Crypto Perpetual Futures Regulation in South America

South America is evolving quickly, with regulators using a mix of securities enforcement, central bank rulemaking, and new registration regimes to pull crypto intermediaries into formal supervision.

For perpetual futures, the pressure points are usually unauthorized offering, stablecoin collateral treatment, and whether local-facing activity triggers licensing or AML obligations.

1. Brazil

Brazil’s securities regulator treats unlicensed crypto derivatives as an authorization issue. In August 2024, the CVM reached a settlement requiring Binance to end an unauthorized derivatives offering, illustrating how quickly offering perpetual products can trigger direct enforcement actions.

In November 2025, the Central Bank of Brazil released long-awaited VASP rules, effective from February 2026, which classify stablecoin transactions as foreign exchange operations. This classification is critical for perp margin collateral, which is predominantly stablecoin-based in the current market.

Prior to this, the Central Bank had been building the post-2022 legal framework through public consultations. Reports in October 2024 indicated that stablecoins and tokenization were high on the agenda, shaping the margin and collateral assumptions that will govern future regulated venues.

2. Argentina

Argentina’s March 2024 reforms pulled crypto intermediaries toward formal registration. CNV Resolution 994/2024 created a PSAV registry covering residents and foreign providers targeting locals, while stressing that registration does not equate to a full CNV operating license.

On the same date, the UIF issued Resolution 49/2024 setting risk-based AML/CTF requirements for PSAVs. For perp brokers, this makes KYC workflows and suspicious-activity reporting a mandatory deliverable, rather than a policy choice, enforcing strict identification standards.

Implementation is ongoing via CNV updates. The CNV’s PSAV registry page states that from May 26, 2025, when General Resolution 1058 entered into force, all new registrations and cancellations must be filed via the Trámites a Distancia (TAD) platform.

3. Colombia

Colombia still lacks a dedicated derivatives perimeter, with cryptoassets treated as digital assets rather than financial instruments. CMS’s country guide notes this leaves activity generally outside central bank and SFC regulation, creating a gap where offshore perps dominate.

Regulatory experimentation occurred through a 2021-2022 sandbox that let banks test crypto rails with exchanges like Gemini and Binance. However, this did not create a standing license for leveraged trading, serving mainly to stress-test KYC and transaction monitoring.

In 2025, policy debate resumed as authorities revisited formalisation efforts, but concrete rules remain unsettled. For perpetual operators, practical risk currently sits in banking access denial, advertising scrutiny, and consumer complaints rather than a clear "derivatives exchange" license.

4. Other South American Markets

Latin American nations are increasingly formalizing their crypto markets, transitioning from unregulated gray zones to structured environments with specific fintech laws.

Notable regulatory developments in other South American jurisdictions include:

- Bolivia: The Central Bank (BCB) recently lifted its long-standing ban, now permitting banks to facilitate crypto transactions and integrate stablecoins for payments.

- Chile: The 2023 Fintech Law empowers the Financial Market Commission (CMF) to supervise crypto exchanges and regulate future stablecoin issuance protocols.

- Venezuela: The national regulator Sunacrip remains in reorganization following corruption scandals, leaving the legal status of crypto derivatives largely uncertain.

- Peru: New legislation mandates that all virtual asset service providers register with the Financial Intelligence Unit to prevent illicit money laundering.

- Paraguay: Legislators are currently debating bills focused primarily on regulating the crypto mining industry rather than establishing clear derivatives frameworks.

- Uruguay: The Central Bank (BCU) is drafting regulations to classify virtual assets as securities, potentially bringing derivatives under existing financial laws.

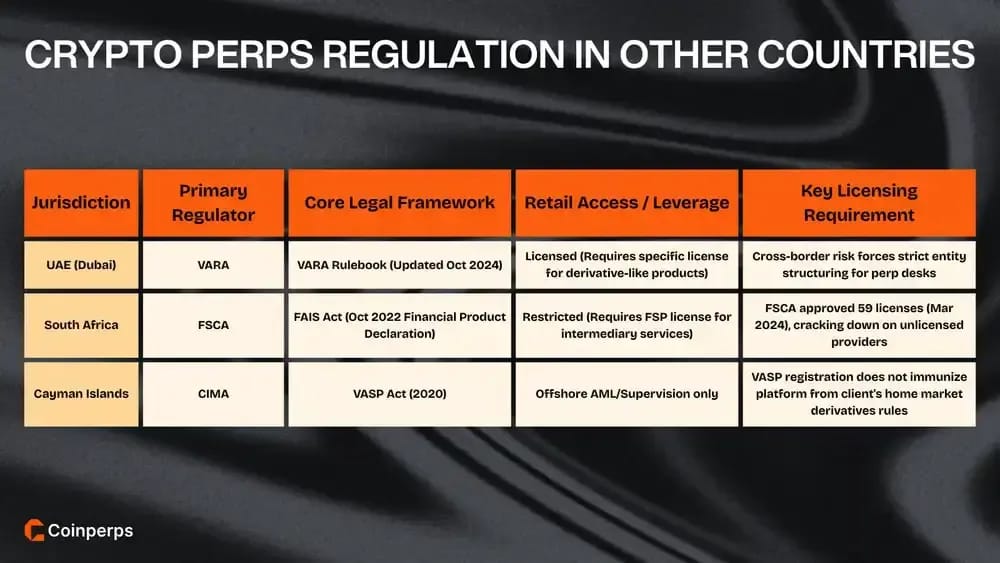

Regulation of Crypto Perpetuals in Other Countries

Outside the Americas, Europe, and Australia, perpetual futures regulation is often defined by a jurisdiction’s licensing architecture for virtual asset service providers plus its legacy derivatives perimeter.

For platforms, the decisive issues are entity location, permitted client types, and whether the rules treat derivatives as a separate regulated activity from spot trading.

1. United Arab Emirates (Dubai)

Dubai regulates market infrastructure through VARA, whose rulebook updated in October 2024 sets licensing expectations for virtual-asset services. This includes specific rules that exchanges and brokers must follow when offering derivative-like products in and from Dubai.

VARA has issued activity-specific rulebooks, such as the May 2023 Licence Code for Virtual Asset Proprietary Trading. These signals indicate that leverage, market making, and custody controls are being split into modular regimes to ensure specialized supervision of high-risk activities.

Cross-border compliance is central due to overlapping regimes like VARA and the ADGM. For perpetual desks, entity structuring and determining "where services are provided from" becomes a critical licensing question, ensuring they do not accidentally trigger unlicensed penalties.

2. South Africa

South Africa moved crypto into mainstream conduct regulation in October 2022 when the FSCA declared crypto assets a "financial product" under the FAIS Act. This means advice and intermediary services around leveraged exposure sit strictly behind a licensing requirement.

The declaration was quickly operationalised, with the FSCA reporting in March 2024 that it had approved 59 crypto licenses. The regulator warned it would act against unlicensed providers, establishing a clear compliance baseline for any perpetual marketing or brokerage.

For offshore perp platforms, the risk is "intermediation." Using local introducers, affiliates, or advisers can cause them to be treated as financial service providers under FAIS, pulling their onboarding and disclosure practices directly into FSCA supervision.

3. Cayman Islands

The Cayman Islands’ VASP Act, introduced in 2020 and later amended, serves as the backbone for licensing many offshore exchanges. However, CIMA’s framework is primarily a supervisory and AML regime for virtual-asset service providers, not a consumer-derivatives rulebook.

Perpetual venues incorporated there still face the "real" derivatives rules in each client’s home market. Cayman licensing helps with banking and governance but does not immunize a platform from CFTC, FCA, or EU MiFID exposure regarding retail distribution.

The practical takeaway is that the regulatory stack is cumulative. Offshore registration provides a corporate home, but it must be paired with hard onshore distribution constraints to avoid enforcement from major jurisdictions targeting the sale of derivatives.

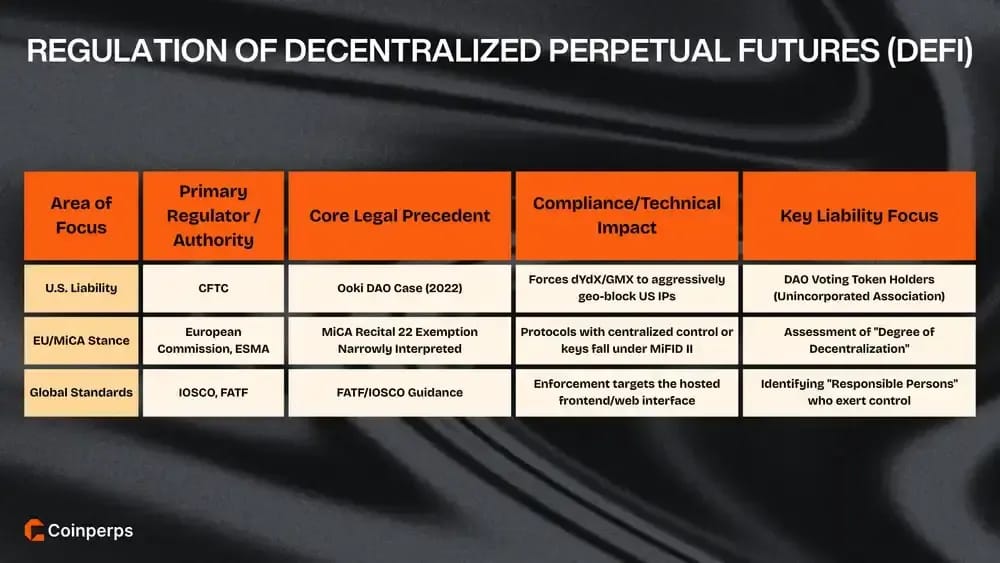

Regulation of Decentralized Perpetual Futures (DeFi)

Decentralized protocols offering leveraged trading now face critical legal exposure worldwide. Regulators are challenging the notion that DAOs and smart contracts can bypass derivatives and AML laws.

In short the current scope of regulations in DeFi perps is:

- US Liability & Ooki DAO: The CFTC established that DAOs are liable as unincorporated associations, shattering "code is law" and forcing protocols to geo-block US users.

- EU MiCA & Decentralization: Regulators narrowly interpret exemptions, subjecting DAOs with centralized teams or keys to full MiFID II licensing and future embedded supervision rules.

- Global Interface Enforcement: Authorities like IOSCO now target web frontends rather than smart contracts, creating a bifurcated market where regulated interfaces require strict KYC compliance.

Bottom Line

Regulators are actively squeezing out high-stakes retail gambling by enforcing tighter leverage caps and demanding rigorous identity checks across major markets.

Yet, stubborn pockets of high-risk trading persist in offshore havens and decentralized protocols that quietly ignore these new compliance burdens.

We expect authorities will soon close these remaining loopholes by aggressively targeting the user interfaces that bridge code and consumer.

Frequently asked questions