Positive vs Negative Crypto Funding Fees Explained

Read our guide on positive vs negative crypto funding fees to find out how these periodic payments influence market prices and your overall trading profits.

Disclosure: Coinperps may earn a commission from partner links, at no extra cost to you. Reviews are based on independent testing, see how we test.

- Crypto funding rates are recurring payment fees exchanged between long and short traders to ensure perpetual contract prices remain closely tied to spot markets.

- Positive fees occur when bulls pay bears during optimistic trends, while negative fees involve bears paying bulls when bearish market sentiment prevails globally.

- These funding rate fees offer valuable sentiment signals and arbitrage income, yet they can also trigger liquidations or erode profits if holding costs become expensive.

Have you ever wondered why your trading account balance fluctuates even when prices remain stagnant? These charges are crypto funding fees, essential mechanisms designed to stabilize perpetual markets. They exist to bridge the gap between perps and spot assets.

In this guide, we explain how these payments function and impact your overall profitability. Understanding the shift between positive and negative rates helps you navigate volatile trends. We provide the tools needed to master these complex derivative market costs.

Read our detailed overview of funding mechanisms below. ⬇️

Positive vs Negative Crypto Funding Fees Overview

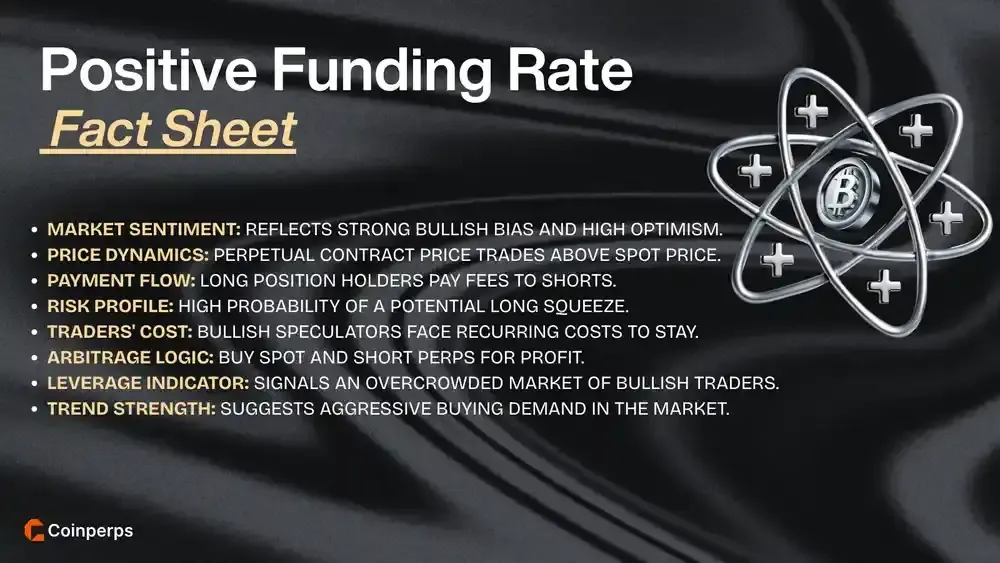

Crypto funding rates are periodic payments exchanged between long and short traders to keep perpetual contract prices aligned with spot markets. When the rate is positive, long positions pay shorts, indicating a bullish bias where the market price exceeds spot.

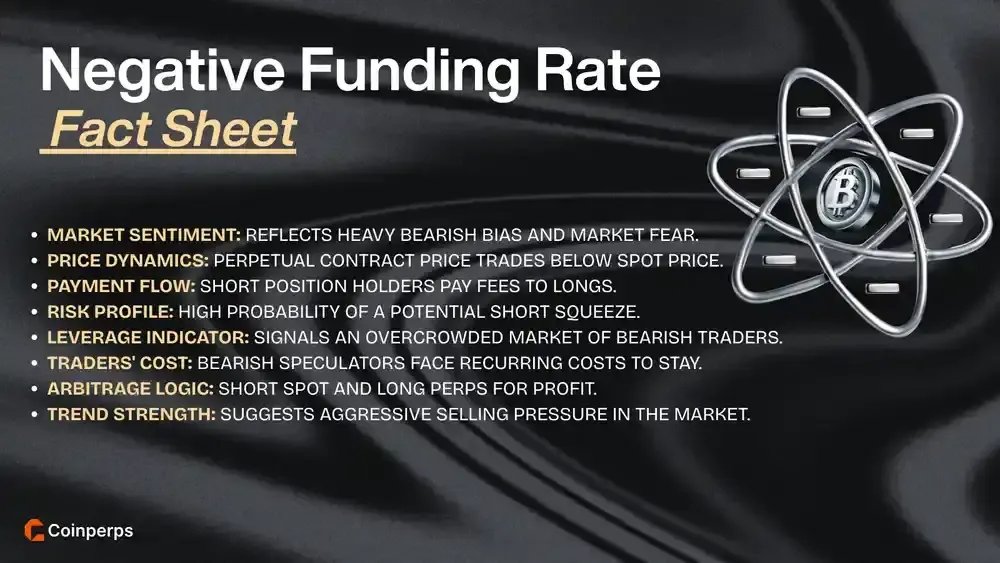

Conversely, a negative rate occurs when the perpetual price stays below the spot value, reflecting bearish sentiment. In this scenario, short sellers pay longs to maintain their positions. This mechanism ensures price stability by incentivizing the less popular side.

The table below breaks down the core distinctions between these two states:

Market Implications of Funding Rates

Funding rates serve as a vital pulse check for market sentiment and leverage health. By analyzing these payments, traders can identify whether the current price action is driven by sustainable buying or overextended speculative positions prone to liquidation.

1. Positive Crypto Funding Fees

Positive rates signal a market dominated by bullish speculation, where the demand for long leverage pushes perpetual prices above spot. While this confirms upward momentum, excessively high rates suggest the trend is becoming expensive and risky for late buyers.

When funding stays high for too long, the "cost of carry" eats into profits, making longs vulnerable to slight price dips. This environment often precedes a long squeeze, as traders exit positions simultaneously to stop paying the recurring fee.

Example: Bitcoin bulls paying $100 daily per contract in fees may eventually sell, causing a price drop that liquidates other over-leveraged long positions.

2. Negative Crypto Funding Fees

Negative rates highlight a bearish environment where shorts are paying longs to keep their positions open. This reflects deep pessimism or heavy hedging, indicating that the majority of market participants are betting on further price declines.

Deeply negative funding is often a "coiled spring" for a short squeeze. Because shorts must pay fees while prices stay flat or rise, they are incentivized to close, which requires buying back assets and driving prices higher.

Example: During a panic, Ethereum shorts paying 0.1% every 8 hours might be forced to buy back quickly if the price starts recovering.

How Are Crypto Funding Rates Calculated?

Exchanges calculate funding rates using a formula combining the interest rate and the premium index. This calculation measures the price gap between perpetual contracts and spot markets. Settlement typically occurs every 8 hours on most major perpetual exchanges.

The premium index tracks how far the perpetual price deviates from the index price. When the gap widens, the funding rate adjusts to incentivize traders to close it. Some platforms now offer settlement every 1 hour for higher precision levels.

You can use our calculator below to estimate your upcoming fees:

Pros and Cons of Crypto Funding Rates

Crypto funding rates provide essential structural benefits to derivative markets while introducing operational hurdles. Examine the core advantages and drawbacks of the funding fee system below:

Top Strategies for Managing Funding Fees

Traders must proactively manage funding costs to protect their profit margins. By employing specific tactical approaches, investors can mitigate high expenses or even profit from them.

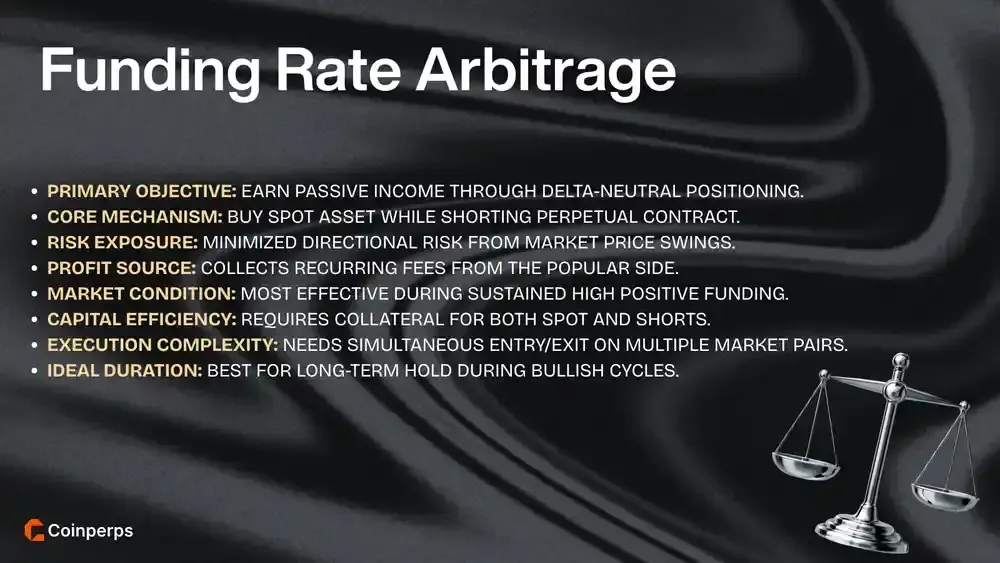

1. Funding Rate Arbitrage

Funding rate arbitrage involves maintaining a delta-neutral position by balancing a perpetual contract against a spot market trade. This strategy allows investors to collect funding payments while remaining protected from the underlying asset's price movements throughout the trade duration.

By longing the spot asset and shorting the corresponding perpetual swap, traders earn positive funding fees without directional risk. This method is popular among institutional players seeking steady yields during bullish phases when funding rates remain consistently elevated.

Example: A trader buys 1 Bitcoin on the spot market and simultaneously opens a 1 Bitcoin short position on a perpetual exchange. They collect the 0.01% funding fee every 8 hours while the total portfolio value remains stable regardless of price.

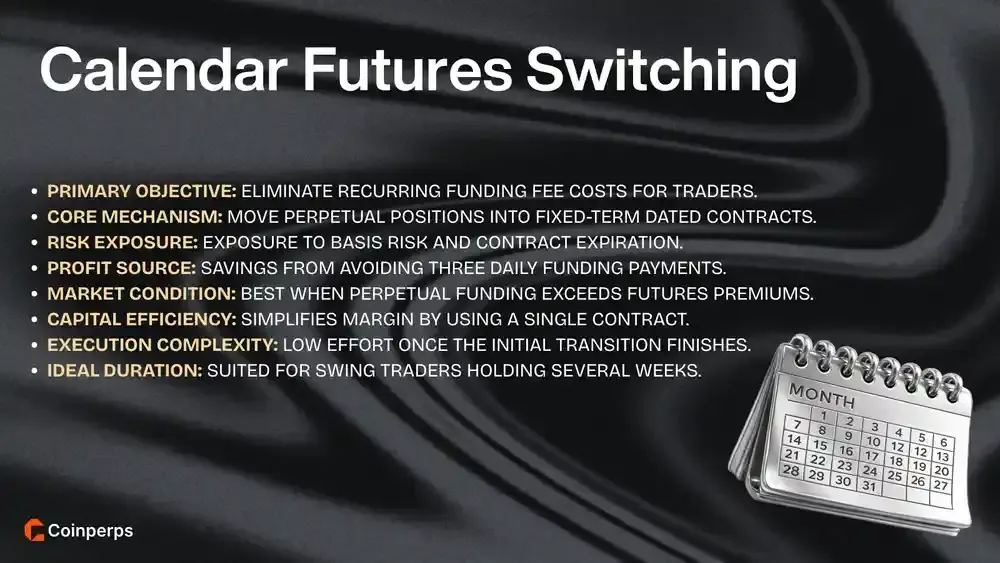

2. Switching to Calendar Futures

When perpetual funding rates become excessively high, traders can switch their exposure to fixed-term calendar crypto futures. Unlike perpetual swaps, these contracts do not utilize funding fees to maintain price parity, instead trading at a premium or discount to spot.

By moving positions into quarterly or monthly futures, investors avoid the recurring "tax" of daily funding payments. This is particularly beneficial for long-term swing traders who intend to hold their directional bias for several weeks or months at once.

Example: An investor holding a large long position in Ethereum perpetuals notices that annual funding costs are exceeding 30%. They close the perpetual trade and open a quarterly futures contract to eliminate those three daily fee payments.

3. Monitoring Sentiment Reversals

Smart traders monitor funding rate extremes as signals for potential trend exhaustion and market reversals. When rates reach historical highs or lows, it often indicates that the current trend is overextended and a liquidation event may be approaching soon.

Reducing leverage or tightening stop-losses during these periods protects capital from the volatility of a squeeze. Successful participants use funding data as a contrarian indicator, preparing for mean reversion when the cost of maintaining a trade becomes unsustainable.

Example: Seeing the Bitcoin funding rate spike to 0.05%, a trader realizes that a long squeeze is likely. They reduce their leverage from 10x to 2x and move their stop-loss closer to the current market price.

Risks of Funding Rates in Crypto Trading

Trading with funding rates introduces specific financial dangers that can erode capital or trigger liquidations. Understanding these threats is vital for any serious investor.

The following list details the primary risks associated with these fees:

- Liquidation Acceleration: High funding fees reduce available margin, which can move liquidation prices closer to market levels and force unwanted position closures during volatility.

- Profit Erosion: Ongoing payments for maintaining a position can significantly diminish realized gains, turning a successful directional trade into a net loss over time.

- Slippage During Squeezes: Rapid market reversals caused by funding extremes often lead to low liquidity, resulting in heavy slippage when trying to exit crowded trades.

- Sudden Rate Spikes: Unexpected changes in market sentiment can cause rates to jump instantly, catch traders off guard with high costs they did not anticipate.

- Unfavorable Settlement Times: Fees are deducted regardless of trade duration, meaning entering a position just before the settlement window triggers a full payment immediately.

- Exchange Rate Discrepancies: Different platforms utilize varying calculation formulas, which can lead to higher costs on one exchange compared to another for identical assets.

- Counterparty Risk: In decentralized environments, the smart contracts managing these payments might have vulnerabilities, potentially leading to a loss of funds or incorrect distributions.

- Psychological Pressure: The constant pressure of paying recurring fees often forces traders into making emotional decisions, such as closing winning trades too early.

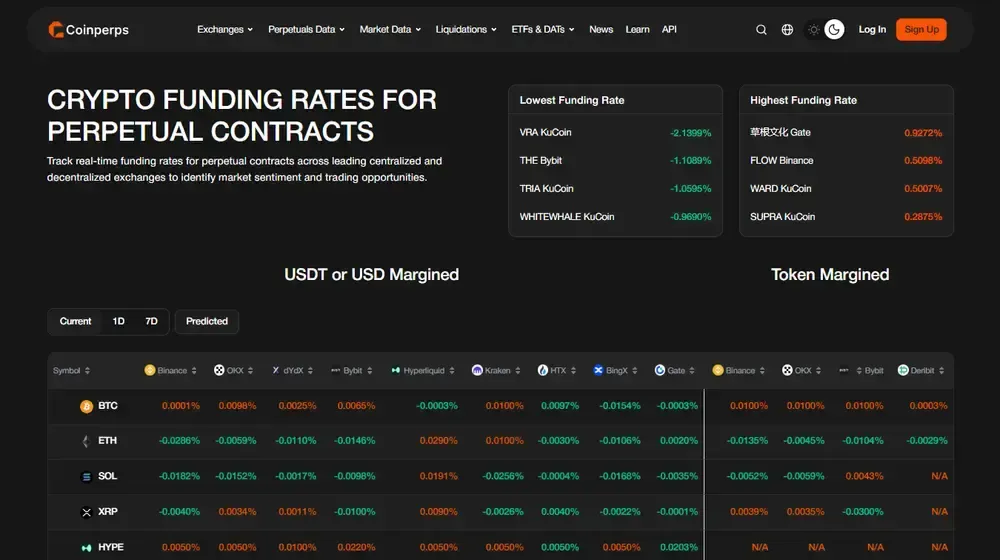

How to Analyze Funding Rates With Coinperps

Analyzing funding rates requires a centralized view of market sentiment across various trading venues. Coinperps provides a comprehensive dashboard that aggregates data from top centralized and decentralized exchanges, allowing traders to spot cross-platform discrepancies and broad trends.

By navigating to the main funding rates page, users can instantly identify the highest and lowest rates across the entire market. This high-level view helps pinpoint which assets are facing extreme speculative pressure and where arbitrage opportunities might be forming.

For deeper asset-specific analysis, the Bitcoin perpetuals page integrates funding data with open interest and liquidation levels. Observing the weighted funding rate alongside volume fluctuations allows traders to distinguish between healthy price discovery and overleveraged positions prone to volatility.

The platform also provides historical charts and predicted rates, which are essential for forecasting upcoming payment obligations. Examining these metrics enables investors to predict changes in settlement and modify their leverage tactics before periods of high costs affect their profitability.

Bottom Line

Funding fees are essential tools that stabilize perpetual markets by aligning contract prices with spot values through periodic installments between long and short traders.

Positive rates indicate bullish demand while negative rates signal bearish sentiment. Monitoring these trends helps investors identify potential market tops or imminent short squeezes.