MiCA Licensed Exchanges: Top CASP-Authorised Platforms

The exchanges that can legally hold your euros after 1 July 2026, ranked by regulator, licence scope and what a verified EU account actually gets you.

Fact checked

Key Takeaways:

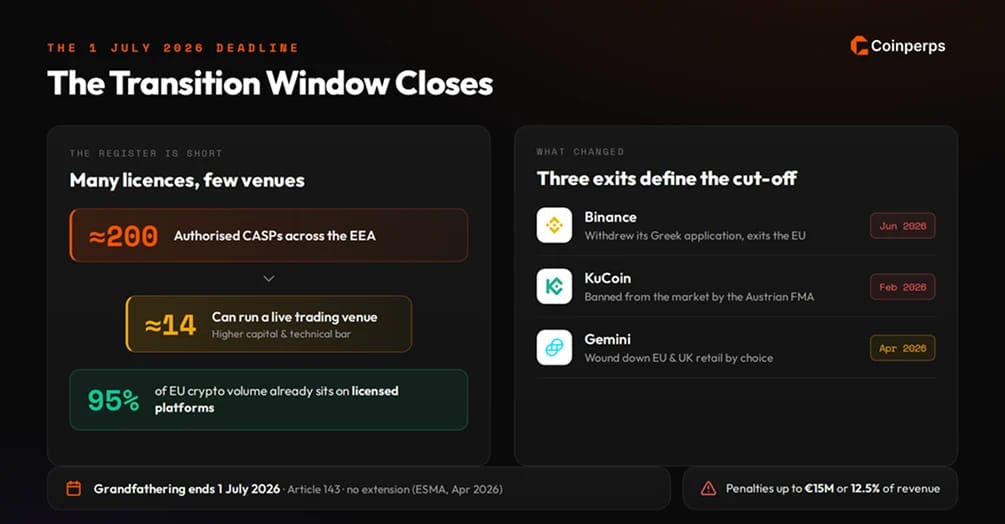

- The transition window closes, and the register is short: From 1 July 2026, serving an EEA resident without a MiCA crypto-asset service provider (CASP) licence breaks EU law. Around 200 firms hold one, only about 14 can run a live trading venue, and licensed platforms already handle close to 95% of EU crypto volume.

- A MiCA licence covers spot and custody, not leverage: Perpetual futures are financial instruments under MiFID II, so a CASP licence alone cannot offer a perp. Only Kraken and OKX here run regulated EEA derivatives today, both capped at 10x.

- The stablecoin menu is re-railed: MiCA only lets licensed venues list stablecoins from authorised e-money issuers, so USDT is delisted for EU retail while Circle's USDC and EURC become the default dollar and euro rails.

The 7 Best MiCA Licensed Exchanges in 2026

Every platform below appears in the ESMA register of authorised CASPs, the only list that legally matters once the grandfathering window shuts.

We ranked them for a leverage-minded audience, weighting licence depth, whether a verified EEA account reaches regulated derivatives, EUR funding and brand strength. Scopes come from each exchange's home authority, cross-checked against the register, per our ranking methodology.

1. Bybit EU

Bybit EU operates under a full crypto-asset service provider licence from Austria's FMA. That authorisation under Article 63 of MiCAR covers custody, exchange of crypto for funds, exchange for other crypto, placing and transfer services, five of the ten regulated activities. It passports across 29 EEA states, with Malta the one member excluded at launch.

With no MiCA-compliant USDT, Bybit EU runs its euro and dollar markets on the Quantoz stablecoins USDQ and EURQ. It publishes independently verified Proof of Reserves and passed regulator-grade penetration testing for the FMA and DORA resilience rules.

It earns the top slot by pairing that licence with the biggest brand in the space. The European entity runs spot, margin, Earn and the Bybit Card on regulated rails, backed by deep liquidity and a compliance-first posture. A real Austrian licence and a mature, well-capitalised operator are what put it ahead of the field.

Pros

- Verified Austrian FMA licence, recourse through the FMA and EU courts, segregated client assets.

- Biggest global derivatives brand inside a MiCA-compliant entity, with a stated MiFID roadmap.

- Independently verified Proof of Reserves and DORA-aligned security testing.

Cons

- Spot and margin only, so no perpetuals for EEA users yet.

- USDT gone, and USDQ and EURQ liquidity is thinner than global USDT books.

- Malta residents not served at launch despite being in the EEA.

2. Kraken

Kraken is the sharpest choice for regulated leverage in Europe today. It is one of very few exchanges holding both licences that matter, a MiCA CASP through the Central Bank of Ireland and a MiFID II derivatives permission through Cyprus's CySEC. Ireland set one of the stricter bars in the bloc, demanding real operational presence over letterbox offices, so the licence carries weight.

It runs what it calls the largest European perpetual offering, 300-plus pairs at the regulated 10x ceiling, settled through its MiFID entity behind an appropriateness test. Crypto collateral has been accepted alongside fiat since late 2025.

Operating since 2011 with no client-fund breach, quarterly Proof of Reserves and SOC 2 Type 2, it is the most complete regulated stack here.

Pros

- Holds both a MiCA CASP and a MiFID II derivatives licence, which is rare.

- Live regulated EU perpetuals, 300+ pairs at up to 10x, with crypto collateral.

- Long operating history, SEPA Instant funding, independently verified reserves.

Cons

- Leverage capped at the regulated 10x, well below offshore venues.

- The appropriateness assessment adds friction for first-time derivatives users.

- Spot fees run higher than the cheapest venues.

3. OKX

OKX holds one of the widest CASP authorisations in Europe, cleared for nine of the ten regulated services by the Malta Financial Services Authority and among the first on the register in January 2025. A MiFID II licence bought through a Maltese entity and a Payment Institution licence for the OKX Card and OKX Pay give it a three-layer stack few rivals match.

For perp traders, the draw is X-Perps, OKX's regulated European derivative launched in April 2026. A true perpetual cannot exist cleanly under MiFID II, since a dateless leveraged product falls into the contract-for-difference bucket ESMA has restricted for retail since 2018. OKX attaches a five-year expiry while keeping the funding rate, turning a perp into a compliant future.

Client assets sit in segregated custody under MiCA's Article 70, and OKX publishes monthly proof of reserves verified with zk-STARK cryptography. Its €1.1 million Maltese AML penalty from 2023 is the caveat, a sign that authorisation lifts the baseline without guaranteeing a spotless record.

Pros

- One of the broadest CASP scopes in the register, plus MiFID II and a Payment Institution licence.

- Regulated X-Perps live for eligible EEA users, with appropriateness checks and negative balance protection.

- Deep global liquidity behind a compliant European wrapper, with segregated client assets.

Cons

- The five-year expiry framing confuses traders expecting a pure perpetual.

- Leverage sits at the regulated European ceiling, not the offshore range.

- A past Malta AML penalty shows the compliance record is not spotless.

4. Coinbase

Coinbase made Luxembourg its MiCA home with a CASP authorisation from the CSSF, one of the bloc's more capital-markets-minded regulators. As a US-listed company reporting quarterly, it offers disclosure no private exchange here can match, the default pick for users weighting regulatory certainty above cost or leverage.

Derivatives run through a separate MiFID-registered entity offering futures across two dozen-plus European countries, and the Deribit acquisition adds options-and-futures infrastructure. Fees run high against trading-focused venues, and the simple buy-and-sell interface hides the cheaper advanced order types. It suits traders who value a publicly audited counterparty and clean compliance over rock-bottom cost.

Pros

- Full CASP authorisation from Luxembourg's CSSF with a public-company disclosure record.

- MiFID-registered futures across much of the EEA, plus a deeper derivatives stack after Deribit.

- Beginner-friendly onboarding and reliable EUR rails.

Cons

- Headline fees are among the higher rates unless you use the advanced interface.

- Retail perpetual access in the EU stays narrower than Kraken or OKX.

- Product depth for active derivatives traders still trails the specialists.

5. Crypto.com

Crypto.com holds its MiCA CASP authorisation through Malta, building on an earlier class-three VFA licence and an e-money institution licence. That payments-plus-exchange base powers its spending card and broad retail suite.

For a leverage-focused reader, this is more a spot and custody venue than a derivatives destination, with limited regulated perp access next to the MiFID-equipped names above. The appeal is breadth and everyday usability, a wide asset menu, a widely used card, and fiat rails. Treat it as an all-round regulated account, not a perp terminal.

Pros

- MiCA CASP plus an e-money licence through Malta, supporting card and payment features.

- Broad retail product suite and a well-known consumer brand.

- Segregated client assets and passported EEA access.

Cons

- Regulated EU derivatives access is limited relative to the top of the list.

- Spread and fee structures on simple flows can be opaque.

- Better suited to spot and spending than active leveraged trading.

6. Gate

Gate runs its European entity under a Maltese CASP authorisation, one of the large exchanges that chose the MFSA. Its calling card is range, one of the widest spot asset selections of any centralised venue, a useful regulated home for early access to smaller-cap names.

The European entity is spot and custody, not a regulated perp venue, so leverage-seekers pair it with a MiFID-equipped name above. Reserves are published regularly, and the passported licence gives EEA users the same segregated-asset protections as the rest. As a compliant altcoin account it does a specific job well.

Pros

- MiCA CASP authorisation via Malta with passporting across the EEA.

- One of the widest spot asset menus on a licensed platform.

- Regular reserve disclosures and segregated client funds.

Cons

- No regulated European perpetual offering, so it is spot-first for EEA users.

- The sheer breadth of listings means more due diligence on thinner markets.

- Best used as a secondary altcoin account, not a primary trading venue.

7. WhiteBIT EU

WhiteBIT EU is the most recent name here, authorised by the Austrian FMA on 19 June 2026, days before the deadline. The licence sits with WB-Shield Innovations GmbH in Vienna and covers custody, crypto-to-fiat and crypto-to-crypto exchange, placing and transfer. Its published scope centres on those services rather than trading-platform operation, narrower than a headline exchange licence. Like Bybit EU, it passports across the EEA with Malta excluded.

WhiteBIT has run one of Europe's larger order books since 2018 and, as part of W Group, reports over 35 million customers worldwide, with sponsorships spanning Visa, FC Barcelona and Juventus. The regulated arm is spot and custody for now, without the MiFID II layer leverage requires, and the whitebit.eu platform is still rolling out to EEA users rather than fully live.

For traders who want depth on major pairs inside a licensed Austrian entity, it is a credible late entrant to watch as its scope matures.

Pros

- Fresh MiCA CASP authorisation from the Austrian FMA, passported across the EEA.

- Deep liquidity on major pairs relative to its size.

- Segregated client assets and EUR funding support.

Cons

- No MiFID layer yet, so no regulated European perpetuals.

- A newer authorisation with a shorter compliance track record inside the perimeter.

- Product scope for EEA users is narrower than the established names.

Why a MiCA Licence Does Not Let You Trade Perps in the EU

MiCA governs crypto-assets that are not already financial instruments, meaning spot tokens, stablecoins, custody and exchange. Perpetual futures are derivatives, and derivatives sit under MiFID II. A CASP licence, however broad, cannot put a perp on your screen without a separate MiFID II investment-firm permission.

An exchange can be fully MiCA-authorised, hold your euros legally, and still be barred from offering leverage. It is why Kraken acquired a Cypriot MiFID entity, OKX bought a Maltese one, and Bybit EU trades spot while its perp ambitions wait on a second application. As of mid-2026, few hold both licences and run live EEA derivatives.

The product itself carries a second constraint. A dateless leveraged product reads as a contract for difference under MiFID II, which ESMA has restricted for retail since 2018, so venues engineer around it. OKX attaches a five-year expiry to keep the funding rate while shedding the CFD label, and Kraken spent months convincing CySEC and ESMA its contracts are exchange-traded products.

The classification is not settled, with the European Commission consulting on whether perps belong under MiFID or MiCA and responses due in late August 2026. Our best crypto futures platforms in Europe guide covers every regulated venue, and our perpetuals versus futures explainer unpacks why that expiry date matters.

The 1 July 2026 Deadline and What Changed

Under Article 143 of MiCAR, firms operating under national law could keep serving EU clients through an 18-month grandfathering window closing 1 July 2026. Several states shortened theirs, Germany and Ireland to end-2025 and the Netherlands to mid-2025, and ESMA confirmed in April 2026 there would be no extension. From today, a platform without a CASP authorisation is outside EU law, facing penalties up to €15 million or 12.5% of annual revenue.

The market that emerges is smaller and more concentrated. Around 200 firms hold full CASP authorisation, yet only about 14 can operate a live trading venue, which carries higher capital and technical bars than custody or brokerage. Germany holds close to a third, ahead of the Netherlands, France and Malta, though the largest consumer exchanges clustered in Malta, Luxembourg and Austria. Licensed platforms already handle an estimated 95% of EU crypto volume, so most traders were already inside the perimeter.

Three departures define the cut-off:

- Binance withdrew and is exiting the EU. The world's largest exchange filed through a Greek subsidiary, saw the Hellenic Capital Market Commission move toward rejection, and pulled the application in June 2026. It leaves the bloc today while signalling it will apply elsewhere.

- KuCoin was banned. The Austrian FMA barred KuCoin from the market in February 2026, closing that route entirely for EEA users.

- Gemini walked away by choice. Despite holding both a MiCA and a MiFID licence, Gemini wound down its UK and EEA retail operations in April 2026, a reminder that a licence is a permission to operate, not an obligation to stay.

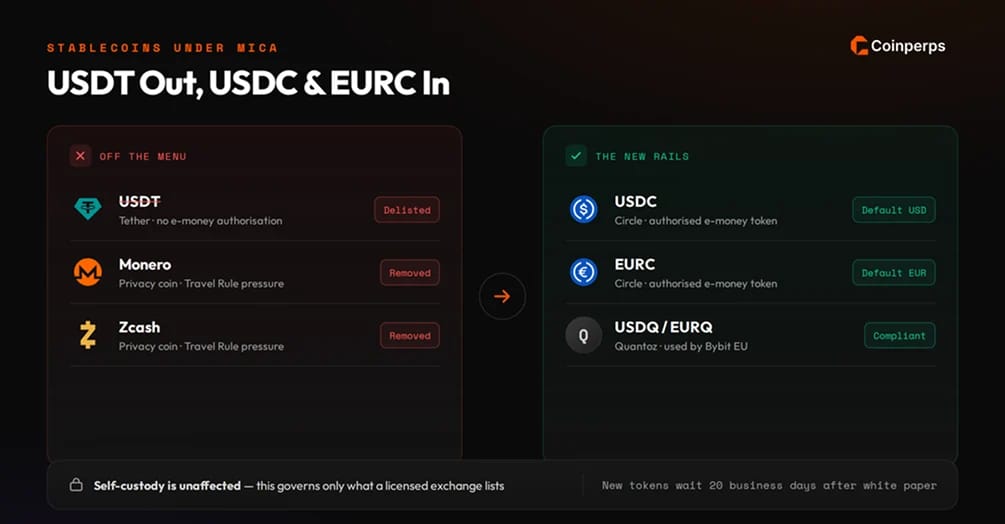

Stablecoins Under MiCA: USDT Out, USDC and EURC In

The most visible change on a compliant European order book is what is missing. MiCA treats stablecoins as e-money tokens, and the issuer needs its own authorisation for the token to trade on a licensed venue. Tether never pursued that for USDT, so Coinbase, Kraken, Crypto.com and Binance's EU entity pulled USDT pairs for retail users ahead of the deadline. It may survive in custody-only mode, but not as a trading pair.

The authorised replacements are Circle's USDC and EURC, now the default dollar and euro rails, alongside other regulated e-money tokens. Bybit EU went its own way with the Quantoz-issued USDQ and EURQ. Privacy coins like Monero and Zcash also came off most major CASPs under Travel Rule and AML pressure, and a newly listed token now waits 20 business days after its white paper before trading.

None of that restricts self-custody. It only governs what a licensed exchange will list.

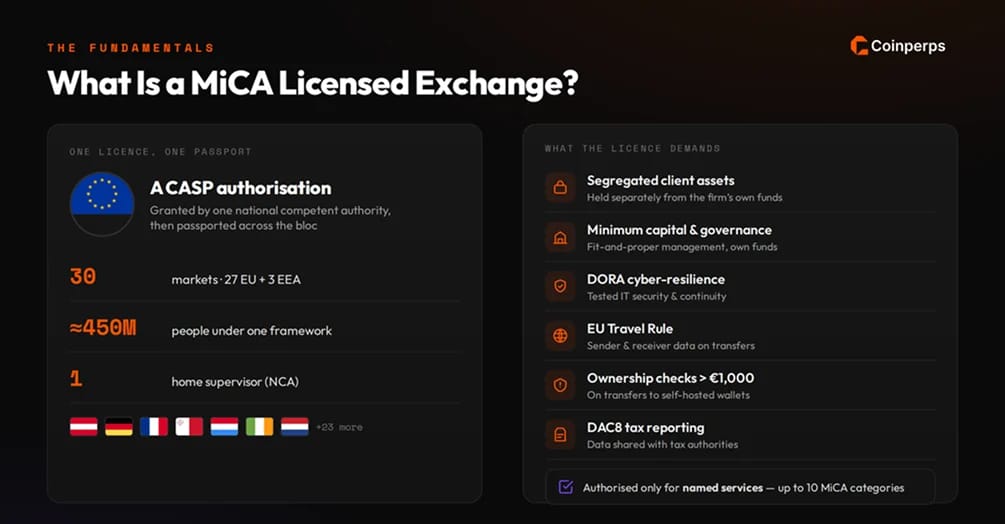

What Is a MiCA Licensed Exchange?

A MiCA licensed exchange holds a crypto-asset service provider authorisation from a national competent authority in one EU or EEA state. This is no light-touch registration. It follows a full review of governance, capital, management suitability, IT security and anti-money-laundering controls, and it names which of MiCA's ten service categories the firm may offer.

The power sits in passporting. A CASP authorised in any single member state can serve all 27 EU countries plus Iceland, Norway and Liechtenstein, roughly 450 million people, under one supervisor. That let exchanges shop for a home regulator, with Malta, Luxembourg and Austria the busiest hubs and Ireland setting a stricter bar.

A licensed venue must segregate client assets, hold minimum capital, run documented cybersecurity procedures, meet DORA resilience rules, apply the EU Travel Rule, and verify ownership on transfers above €1,000 to a self-hosted wallet. DAC8 added automatic tax reporting, so providers now pass client transaction data to national tax authorities. Our perpetual exchange regulation explainer covers how these rules land across centralised and on-chain venues.

How to Verify a MiCA Licence

Do not take a homepage badge at face value. A two-minute check protects your capital and your legal standing.

- Find the exact legal entity. Confirm the company serving you, such as Bybit EU GmbH or OKX Europe Limited, not the parent brand. Licences attach to entities, not logos.

- Search the ESMA register. Look the entity up in ESMA's public register of authorised CASPs, republished weekly. If it is not listed, treat that as a red flag.

- Read the licensed services. A CASP is authorised for named activities only, so confirm the venue holds the service you need, whether custody, exchange or trading-platform operation.

- Separate MiCA from MiFID. If you want leverage, check for a MiFID II permission on top of the CASP licence. Spot authorisation says nothing about perps.

Risks and Considerations

A licence removes some risks and leaves others in place. The list below covers what still applies inside a regulated venue.

- A licence is a floor, not immunity. OKX carried a €1.1 million Maltese AML penalty while fully authorised, so authorisation raises the baseline without certifying a flawless record.

- Regulated leverage is capped. European retail perps top out at 10x under MiFID appropriateness rules, so offshore-style leverage will not appear on a compliant venue.

- Stablecoin and asset menus are narrower. USDT pairs, privacy coins and freshly listed tokens are restricted or delayed, which changes how you fund and what you can trade.

- Migration is not automatic. Moving to a licensed entity such as Bybit EU means fresh KYC even with a verified global account, plus Travel Rule checks on deposits and withdrawals.

- Tax visibility increased. DAC8 reporting means licensed venues now share your transaction data with tax authorities, so record-keeping matters more than it did.

- The rulebook is still moving. The pending Commission consultation on whether perps sit under MiFID or MiCA could reshape derivatives access before year-end.

Bottom Line

The European market opening on 1 July 2026 is smaller and cleaner than the patchwork it replaced. Around 200 CASPs exist on paper, but the ones that matter are the handful pairing a real licence with genuine liquidity. For a straightforward regulated spot and custody account, any of the seven names here will serve you.

For a perpetuals trader, remember the split. A MiCA licence lets an exchange hold your euros, while only a MiFID II permission lets it offer leverage. On that axis Kraken and OKX lead today, with live regulated books capped at 10x. Bybit EU earns the top ranking on the wider view, pairing the deepest global derivatives brand with a compliant Austrian licence and the clearest path to regulated European perps once its MiFID application lands.

Our perpetual exchange rankings and funding rate tracker show how every venue stacks up on live cost and access. Verify the entity on the ESMA register before funding anything, and assume the rules will keep moving.

Frequently Asked Questions

Are crypto funds on a MiCA licensed exchange insured if the platform fails?

No. MiCA has no equivalent of the bank deposit guarantee scheme or the investor compensation scheme that covers cash and securities, so authorisation does not turn your balance into an insured deposit. It relies on strict custody rules instead. A CASP must keep client crypto-assets segregated from its own and is liable for any loss attributable to it, capped at the asset's market value when the loss occurred, unless it proves the cause was beyond its reasonable control.

Can UK residents use MiCA licensed exchanges?

MiCA is EU and EEA law, so it does not cover the United Kingdom. UK users fall under the FCA regime, which runs its own cryptoasset registration and is phasing in a broader authorisation framework. Some MiCA-licensed operators serve UK clients through a separately regulated UK entity while others restrict access, so a UK trader should confirm which entity and licence actually applies before funding an account.

Does MiCA regulate NFTs and DeFi platforms?

Mostly no, with limits. Genuinely unique, non-fungible NFTs sit outside MiCA, but collections issued in large fungible series or tokens that behave like financial instruments can be pulled back in. Fully decentralised services with no identifiable intermediary also fall outside the CASP regime for now, though the European Commission is studying whether DeFi needs dedicated rules.

What is the difference between a CASP and a VASP?

A CASP, or crypto-asset service provider, is the entity authorised and supervised under MiCA across the EU and EEA. A VASP, or virtual asset service provider, is the older anti-money-laundering term from FATF guidance, tied to national registrations rather than a single passportable licence. In practice, a firm that held a VASP registration in an EU state now needs full CASP authorisation to keep operating legally.