Kalshi Perpetuals Review: America's First Regulated Perps

A full review of Kalshi Perpetuals, the first true CFTC-regulated perpetual futures in the US, covering contract specs, funding, margin and how they stack up against offshore venues.

Disclosure: Coinperps may earn a commission from partner links, at no extra cost to you. Reviews are based on independent testing, see how we test.

- Kalshi Perpetuals are the first true perpetual futures approved on a US-regulated exchange. The CFTC cleared the BTCPERP contract on May 29, 2026, Bitcoin went live on June 3, Ethereum on June 4 and XRP on June 10, all USD-settled and tradable 24/7.

- The regulatory plumbing is the product. Trades execute on the KalshiEX designated contract market, margin sits with the Kinetics FCM in customer-segregated accounts earning roughly 3.25% APY, and clearing runs through Kalshi Klear, a CFTC-regulated clearinghouse.

- The trade-off is breadth and leverage. Every new contract needs Commission sign-off, leverage sits well below the 100x-plus common offshore, and apps run isolated margin only, so traders chasing long-tail listings will still look at venues like Hyperliquid.

Until this month, an American trader who wanted a perpetual future had two options: break the rules or leave the country. Offshore perp volume climbed from $28 trillion in 2023 to more than $90 trillion in 2025, and essentially none of it touched a US-regulated order book. Kalshi just changed that.

On June 3, 2026, the prediction-market exchange flipped on Bitcoin perpetual futures under full CFTC oversight, branding the product American Perpetuals. This review covers what Kalshi Perpetuals are, how the contracts and margin system work, what they cost, and where they genuinely compete with the offshore giants that built this market.

What Are Kalshi Perpetuals?

Kalshi Perpetuals are USD-margined crypto perpetual futures listed on KalshiEX, the CFTC-designated contract market behind Kalshi's prediction business. The CFTC issued an Order of Approval for the BTCPERP contract on May 29, 2026, reviewed under Commission Regulation 40.3 just one day after submission. The same release confirmed each future perp will face a case-by-case review, and that perpetual designs may not suit every asset class.

One precision point matters for the "first" claim. The CFTC cleared a Bitnomial contract in December 2025 that mimicked perpetual economics, but it carried a 25-year term limit. BTCPERP is the first contract on a registered US exchange with no expiry at all, which is what makes it a genuine perpetual.

The launch cadence has been fast for a regulated venue. Bitcoin opened on June 3, Ethereum on June 4, and XRP went live on June 10 under the XRPPERP ticker, confirmed by RippleX, each carrying a zero-trading-fee promotion for early waitlist users. Kalshi's contract documentation lists 13 crypto assets in the program, including SOL, DOGE, LINK, DOT, LTC, BCH, SUI, XLM, SHIB and HBAR, and on June 9 the company filed with the CFTC for a Hyperliquid (HYPE) perpetual on top of that list. Agricultural commodities are explicitly off the table.

Demand showed up immediately. The waitlist passed one million people, volume cleared $100 million in the first 24 hours, and the contracts crossed $1 billion in total volume within the first week. The launch also caps a big stretch for the company itself, which raised a $1 billion Series F at a $22 billion valuation in May and says it handles more than 90% of US prediction-market activity.

How the Regulated Kalshi Perps Works

Functionally, a Kalshi perp behaves like the contracts traders know from any major venue: long or short with leverage, no expiry, a funding rate anchoring price to spot, and automatic liquidation when margin runs out. What differs is everything underneath the order book, which splits across three regulated entities.

Kalshi's affiliate Kinetic Markets registered as a futures commission merchant with the National Futures Association in March 2026, the licence that makes margin trading possible at all. Customer margin sits in customer-segregated accounts walled off from Kalshi's operating funds, and idle balances earn interest at the clearinghouse, currently around 3.25% APY.

One design choice matters for existing Kalshi users: the perpetuals margin account is fully separate from the predictions balance. Funds move between the two on demand, but a liquidation on a perp position can never drain money sitting in event contracts.

Note: Segregation is the feature offshore venues cannot replicate. When an unregulated exchange fails, customer funds are usually part of the wreckage. Under the CFTC regime, margin is legally not the exchange's money.

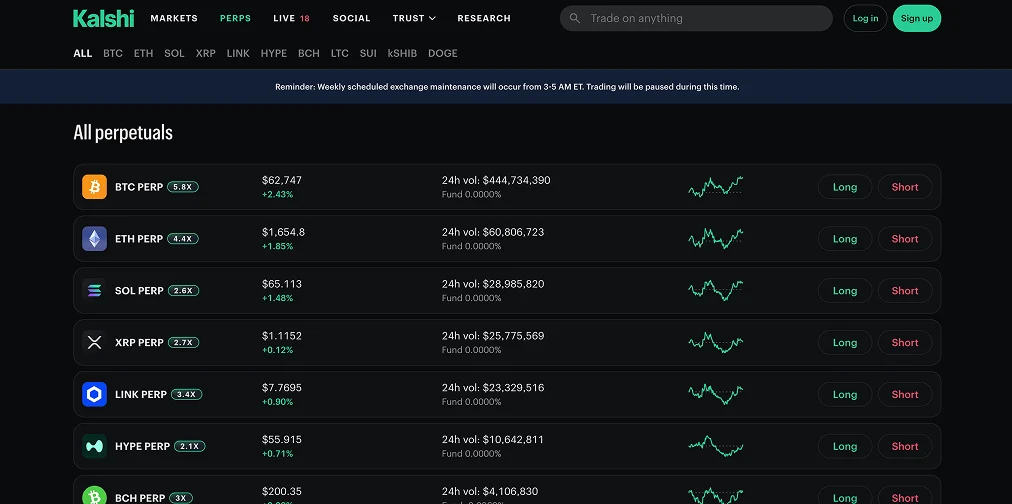

Contract Specs and Available Markets

The contracts are linear and deliberately retail-sized. One BTC contract represents 0.0001 BTC, putting the minimum position near $8 at current prices, and fractional sizing applies across the lineup. Per the BTC contract specification, markets trade 24/7 outside a short weekly maintenance window.

Every contract references a CF Benchmarks real-time index rather than Kalshi's own feed. For Bitcoin that is the BRTI, the same institutional benchmark family used across regulated derivatives globally, aggregated from multiple vetted exchanges and updated every second. Liquidations key off an aggregated mark price designed to resist short-lived wicks on any single venue.

Leverage is set per asset rather than as one headline number, and Kalshi's own education materials work through examples up to 50x while noting limits can change per market. That lands far below the 100x to 125x ceilings standard offshore, which is consistent with how the CFTC has approached retail leverage everywhere else.

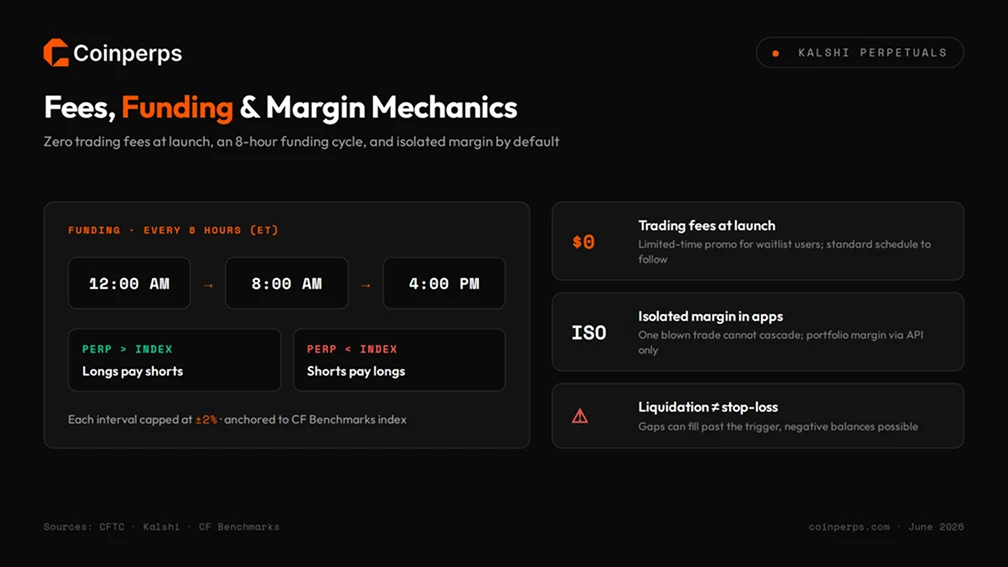

Fees, Funding and Margin Mechanics

Pricing at launch is aggressive: trading fees are zero for early access users for a limited period, with a standard schedule to follow on kalshi.com. The real recurring cost is funding, charged every eight hours and visible line by line in transaction history. The mechanism is the standard one, longs pay shorts when the perp trades above the index and the reverse below it, with each interval capped at plus or minus 2%. You can benchmark those payments against every major venue on the CoinPerps funding rates tracker.

Margin behaves differently from a typical crypto exchange in two ways. First, the consumer apps run isolated margin only, so each position carries its own collateral and a blown trade cannot cascade through the account; cross-style portfolio margin exists but only through the API. Second, take-profit and stop-loss orders are built in, and liquidation triggers when position equity falls through the maintenance threshold against the mark price. Kalshi is direct that liquidation is not a guaranteed stop, and a violent gap can still close a position at a worse price than the trigger, including into a negative balance.

Kalshi vs Offshore and Onchain Perps

Kalshi did not enter an empty field. It entered the most liquid product category in crypto, where perp volume reached $61.7 trillion in 2025, up 29% year on year, and its real pitch is jurisdiction rather than depth. The same week BTCPERP was approved, the CFTC issued a no-action position letting Coinbase route US customers to its Deribit affiliate, creating two parallel onshore paths at once.

Against Hyperliquid the contrast is sharpest, and also the most intertwined. The onchain leader offers no-KYC access, permissionless markets through the framework covered in our HIP-3 explainer, and liquidity Kalshi will need years to approach. Kalshi counters with something Hyperliquid structurally cannot offer Americans: legal access, since US residents are formally restricted from the platform, a situation unpacked in our guide on Hyperliquid access in the USA. Yet the two are partners as much as rivals: Kalshi's regulated markets already run on Hyperliquid's execution layer through the HIP-4 outcome-trading framework, and Kalshi now wants to list a regulated HYPE perp of its own.

Institutions running pensions, endowments and corporate treasuries were never going to touch unregulated venues regardless of depth, and that pool is the one Kalshi is actually fishing in. The listing pipeline is the structural weakness. Because every contract is individually approved, Kalshi launches assets in single digits while offshore books quote hundreds, and you can compare live coverage across venues in the perpetual exchanges directory.

How to Trade Kalshi Perpetuals

Getting a first position open takes five steps, and existing Kalshi prediction users start most of the way there.

- Create and verify an account. Sign up at kalshi.com and complete identity verification, which is mandatory since this is a regulated US futures venue.

- Fund the margin account. Deposit USD via ACH or wire directly into the perpetuals margin account, or transfer from an existing predictions balance in the Portfolio tab.

- Pick a market. Open the Perpetuals section and select a contract, checking the per-asset leverage cap and minimum order size shown on each market page.

- Set the position. Choose long or short, set size and leverage, and attach take-profit and stop-loss levels at entry rather than after the trade moves.

- Manage funding and margin. Watch the 8-hour funding payments on held positions and keep equity comfortably above maintenance margin, since liquidations execute against the mark price automatically. Live positioning data like BTC open interest and funding helps frame whether longs or shorts are paying to hold.

Risks to Consider

A regulated wrapper changes who holds your money, not how leverage behaves. Weigh these before sizing in:

- Leverage cuts both ways. At 50x, a roughly 2% adverse move reaches liquidation, and crypto routinely moves that much in an hour.

- Liquidation is not a stop-loss. Gaps and thin moments can fill a forced close well past the trigger, and a negative balance is possible in extreme conditions.

- Early liquidity is shallow. A week-old order book cannot absorb size the way Binance or Hyperliquid can, so slippage on larger orders will be worse for now.

- The fee holiday ends. Zero trading fees are a launch promotion with no published end date, and the economics change once the standard schedule applies.

- Listings will lag. Per-contract CFTC approval means no long-tail or memecoin perps any time soon, and no agricultural products at all.

- KYC and tax visibility. Every trade sits inside the US regulatory perimeter, which is the entire point, but traders who valued the anonymity of offshore venues lose it here.

Bottom Line

Kalshi Perpetuals are the most consequential US crypto derivatives launch in years, less for the contracts themselves than for the precedent. A perpetual future now exists inside the full CFTC stack, with segregated customer margin, a regulated clearinghouse and interest paid on idle collateral, which is a sentence nobody could write before June 2026.

As a trading venue today, it is a focused tool rather than a replacement for the incumbents. Three live markets, modest leverage, isolated margin in the apps and a young order book mean active traders will keep most of their flow where the depth is. For US-based traders who want leveraged crypto exposure without legal grey zones, and for institutions that could never touch this product class at all, Kalshi is now the default answer.

The bigger question is speed. The first $1 billion took a week, ten more approved contracts are queued behind BTC, ETH and XRP, and a HYPE filing is already with the Commission. If that pipeline keeps moving and liquidity compounds, the offshore monopoly on perps starts looking less permanent than its $90 trillion of volume suggests.

Frequently asked questions

Are Kalshi Perpetuals available outside the US?

Kalshi is built for the US market and requires full identity verification. The product is pitched as American Perpetuals precisely because it gives US residents a domestic, regulated route to an instrument they previously had to access offshore.

How much leverage do Kalshi Perpetuals offer?

Leverage is set individually per asset and shown on each market page, with Kalshi's own materials working through examples up to 50x. That is well below the 100x-plus available on offshore exchanges, reflecting the CFTC-regulated structure.

What fees does Kalshi charge on perpetuals?

Trading fees are zero for early users during the launch promotion, with the standard schedule published on kalshi.com once it ends. Funding payments still apply, exchanged every eight hours at 12:00 AM, 8:00 AM and 4:00 PM ET and capped at 2% per interval.

Can a perp liquidation affect my Kalshi predictions balance?

No. The perpetuals margin account and the predictions balance are held under separately regulated entities and do not share funds, so a liquidation on a leveraged position cannot touch money allocated to event contracts.

Which perpetuals are live on Kalshi right now?

Bitcoin (June 3), Ethereum (June 4) and XRP (June 10) are trading, with ten more assets including SOL, DOGE, LINK and HBAR documented and pending, plus a fresh CFTC filing for a Hyperliquid (HYPE) contract.