Kalshi Restricted Countries (Prediction Market & Perps)

Kalshi is the only CFTC-regulated venue offering both event contracts and crypto perps, and its access map is unusual. The Member Agreement restricts 54 jurisdictions, perps are US-only, and several governments block the platform outright.

Disclosure: Coinperps may earn a commission from partner links, at no extra cost to you. Reviews are based on independent testing, see how we test.

- Bitget restricts roughly two dozen named jurisdictions in 2026, including the United States, Canada, Singapore, Hong Kong, South Korea, and the Netherlands, plus sanctioned states like Iran, North Korea, and Cuba. The count nears 39 once US territories are listed separately.

- KYC is mandatory. Government ID and facial recognition have gated deposits, trading, and withdrawals since January 2024, closing the unverified workaround older guides relied on.

- The license footprint is real but incomplete. Bitget holds El Salvador DASP and BSP licenses, an AUSTRAC registration, and EU national VASP registrations, but no full MiCA CASP and no US entity, leaving it behind OKX, Bybit, Kraken, and Gate.

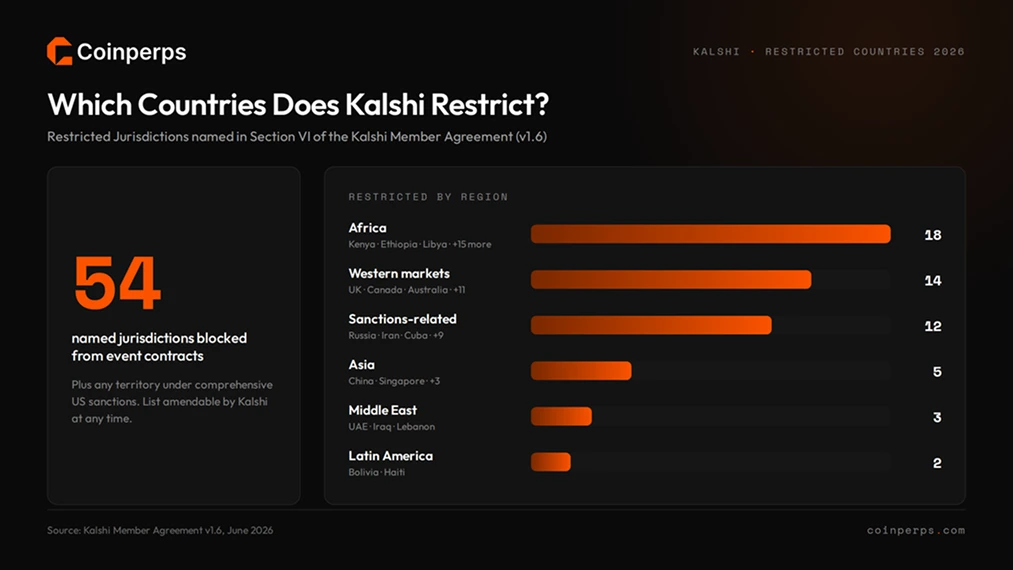

Which Countries Does Kalshi Restrict?

Kalshi's restricted list sits in Section VI ("Representations and Warranties") of the Kalshi Member Agreement, which prohibits event contract trading for anyone domiciled, organized, or located in 54 named jurisdictions, plus any territory under comprehensive US sanctions.

Restricted Jurisdictions as of v1.6 of the Member Agreement:

- Sanctions and conflict-related: Afghanistan, Belarus, Cuba, Iran, Myanmar (Burma), Nicaragua, North Korea, Russia, Syria, Ukraine, Venezuela, Yemen

- Western markets with gambling-law friction: Australia, Belgium, Bulgaria, Canada, France, Hungary, Ireland, Italy, Monaco, New Zealand, Poland, Portugal, Switzerland, United Kingdom

- Asia: People's Republic of China, Laos, Singapore, Taiwan, Thailand

- Middle East: Iraq, Lebanon, United Arab Emirates

- Africa: Algeria, Angola, Burkina Faso, Cameroon, Central African Republic, Côte d'Ivoire, Democratic Republic of the Congo, Ethiopia, Kenya, Libya, Mali, Mozambique, Namibia, Niger, Somalia, South Sudan, Sudan, Zimbabwe

- Latin America: Bolivia, Haiti

The Western entries share one cause. Regulators in the UK, Australia, and the EU's stricter gaming regimes treat wagering on event outcomes as licensed gambling, so those markets were carved out when international signups opened in October 2025. Kalshi raised $300 million at $5 billion alongside that expansion and now sits at a $22 billion valuation after back-to-back $1 billion rounds.

One drafting detail matters. The restrictions "apply solely to the trading of Event Contracts," leaving membership, platform access, and other contract types untouched. The carve-out arrived as Kalshi prepared its perpetuals line, letting the exchange set geographic rules per product. The list is amendable unilaterally, so check the live agreement before signing up.

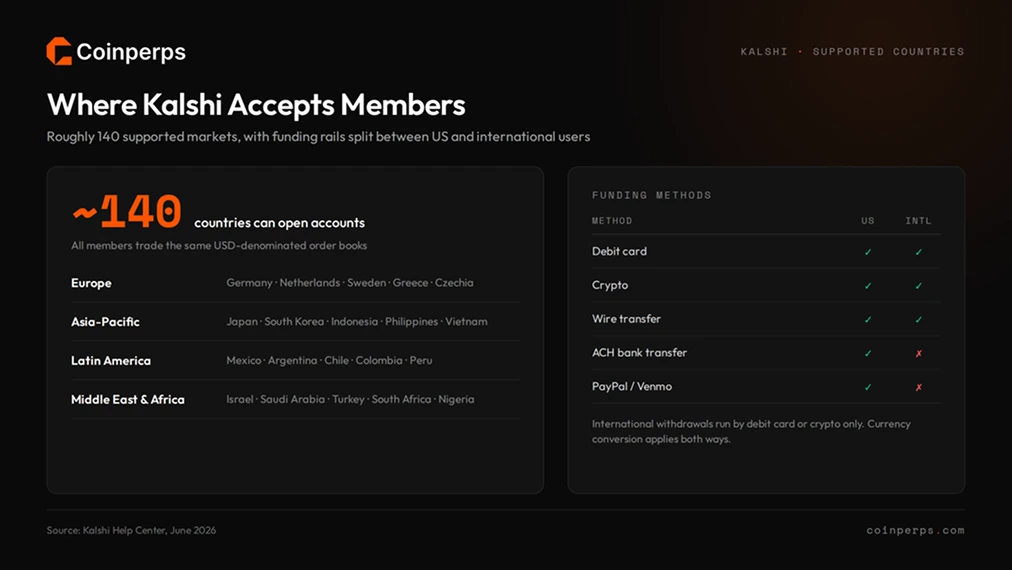

Countries Supported by Kalshi

Outside the Restricted Jurisdictions, Kalshi accepts members from roughly 140 countries, all trading the same USD-denominated order books as American users. Notable supported markets include:

- Europe: Germany, Spain, Netherlands, Austria, Denmark, Sweden, Norway, Finland, Greece, Czech Republic, Romania

- Asia-Pacific: India, Japan, South Korea, Indonesia, Philippines, Vietnam, Malaysia

- Latin America: Brazil, Mexico, Argentina, Chile, Colombia, Peru

- Middle East and Africa: Israel, Saudi Arabia, Turkey, South Africa, Nigeria, Egypt, Morocco

Supported is doing heavy lifting in several of those rows. Spain ordered ISPs to block Kalshi in May 2026, Brazil cut access in April, and India's new online gaming law has put both major prediction platforms in regulators' sights. Membership eligibility and practical access have diverged sharply this year, covered below.

Per Kalshi's help center, international users deposit by debit card, crypto, or wire, and withdraw by debit card or crypto. ACH, PayPal, and Venmo stay US-only. All balances are USD-denominated, so non-US users wear currency conversion both ways.

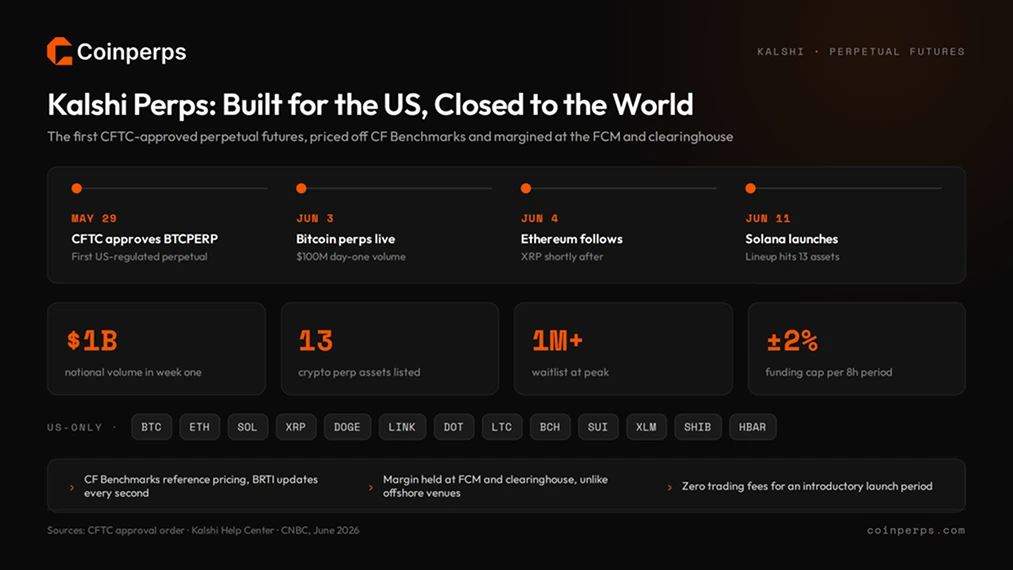

Kalshi Perpetual Futures Restrictions

Kalshi's perps invert the usual offshore-exchange setup. Where venues like BloFin and Hyperliquid serve everyone except the US, Kalshi built a perpetuals product that serves the US first and markets it as "American Perpetuals."

The CFTC issued its approval order for BTCPERP on May 29, 2026, the first perpetual futures contract authorized on a regulated US exchange. Bitcoin went live June 3, Ethereum June 4, and Solana June 11, with the full lineup now covering 13 assets: BTC, ETH, SOL, XRP, DOGE, LINK, DOT, LTC, BCH, SUI, XLM, SHIB, and HBAR. A HYPE contract is filed with the CFTC, and agricultural perps are explicitly off the table.

Structural points that separate the product from offshore perps:

- Reference pricing comes from CF Benchmarks, the KPMG-audited index provider behind CME's crypto futures, with the Bitcoin Real-Time Index updating every second.

- Funding runs every eight hours, capped at plus or minus 2% per period, a tighter band than most offshore venues allow during volatility spikes.

- Margin sits in regulated futures accounts at both Kinetic Markets, Kalshi's affiliated Futures Commission Merchant, and the clearinghouse level, a customer-protection structure no offshore perps venue replicates.

- Leverage is conservative by offshore standards. Kalshi's materials work through liquidation math at 5x and 10x rather than the 100x-plus figures common elsewhere, and limits vary by asset.

Demand was immediate. CNBC reported over $100 million in notional volume in the first 24 hours, $1 billion within a week, and a waitlist that topped one million people, making perps the fastest-growing product in company history. Trading fees are waived for an introductory period. Full contract specs, funding mechanics, and risks are covered in the Kalshi Perpetuals review.

International traders cannot access any of this yet. The launch targets US users, so residents of the 54 Restricted Jurisdictions and most other countries need the venues in the perpetual exchanges directory instead. Coinperps tracks live funding rates and open interest across those alternatives.

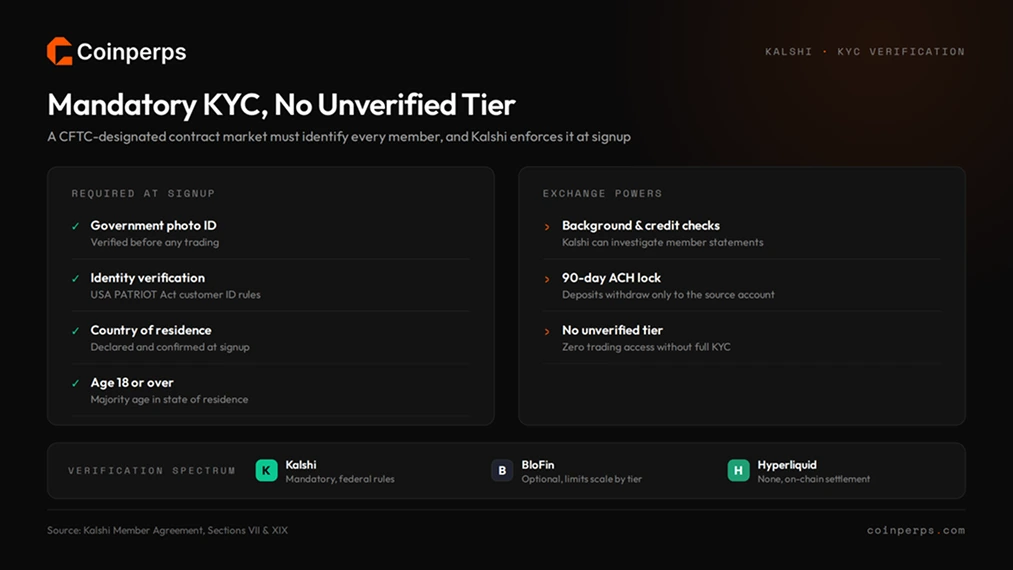

Does Kalshi Require Mandatory KYC Verification?

Yes, with no unverified tier of any kind. As a CFTC-designated contract market, Kalshi falls under the USA PATRIOT Act's customer identification rules, which the Member Agreement spells out directly: the exchange must obtain, verify, and record identifying information for every member.

Signup requires government ID, identity verification, and confirmation of country of residence, and members must be at least 18. Kalshi also reserves the right to run criminal background and credit checks, and ACH-funded accounts can only withdraw back to the originating bank account for the first 90 days. Anyone weighing Kalshi against optional-KYC venues should read the best no-KYC perpetual futures exchanges ranking, because the two models sit at opposite ends of the verification spectrum.

Is Kalshi Banned in the US?

No. The US is Kalshi's home market and the platform is federally legal in all 50 states under CFTC oversight. The fight is at the state level, and it centers on sports contracts.

State gaming regulators in Nevada, New Jersey, Tennessee, Massachusetts, and a dozen others argue that sports event contracts are sports betting wearing a derivatives costume, issuing cease-and-desist orders and lawsuits through 2025 and 2026. Kalshi's counter is federal preemption: a designated contract market answers to the CFTC, not fifty state gaming commissions.

The preemption argument is winning. A federal appeals court sided with Kalshi against New Jersey, holding that the Commodity Exchange Act gives the CFTC exclusive authority over contracts listed on a federally licensed DCM. The CFTC has gone further, suing Arizona, Connecticut, and Illinois to stop them enforcing gambling statutes against prediction markets. Massachusetts courts barred Kalshi's sports contracts and Minnesota passed the first state law banning prediction platforms, so the patchwork is unresolved, but the federal trajectory favors the exchange. The 2026 World Cup, running across the US through July, has pushed sports contract volume and regulatory attention up together.

Which Countries Have Banned Kalshi?

This is the newest layer in Kalshi's access picture and the one older guides miss. Kalshi's restricted list describes who the exchange turns away. A growing list of governments now describes who turns Kalshi away, and the two barely overlap.

- Brazil blocked Kalshi and Polymarket in April 2026 in an action covering more than two dozen platforms, with the central bank ruling event contracts non-compliant with local derivatives rules. The block landed weeks after Kalshi entered Brazil through a partnership with brokerage XP, the most abrupt reversal of the year.

- Spain ordered internet providers to block both platforms on May 26, 2026, with the DGOJ gambling regulator opening disciplinary proceedings over unlicensed betting. The block is precautionary while the case runs, expected to take three to four months.

- India brought prediction markets under the Promotion and Regulation of Online Gaming Act, in force since May 1, 2026, classifying them as prohibited online money gaming. A blocking order hit Polymarket on May 21 with a parallel Kalshi order reported in preparation.

The common thread is definitional. Kalshi argues it operates a financial market where prices aggregate probability. The regulators acting against it have all concluded the product is unlicensed gambling. Until a jurisdiction outside the US builds a recognized category for event contracts, expect this list to grow faster than Kalshi's own list shrinks.

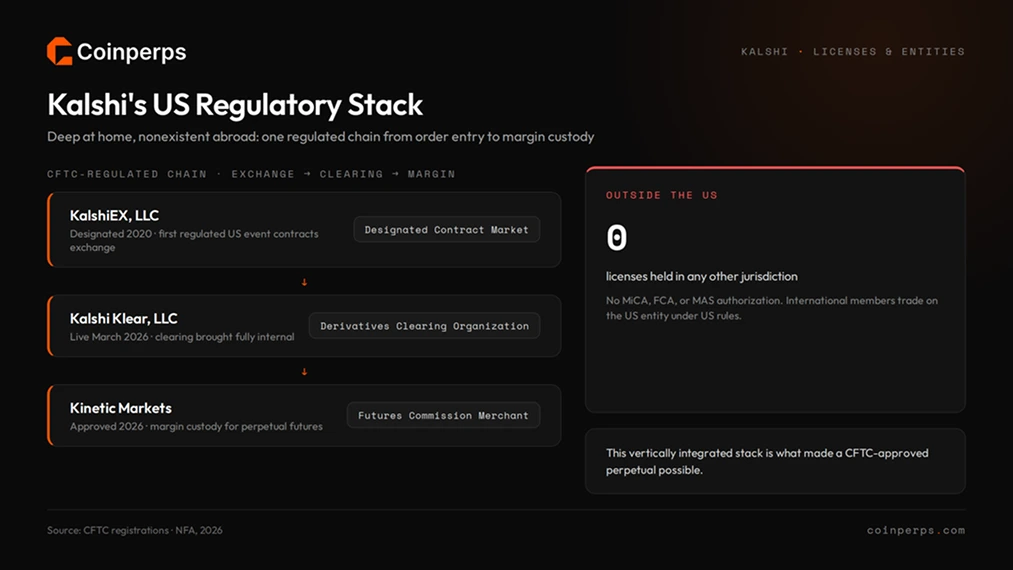

What Licenses Does Kalshi Have?

Kalshi's regulatory stack is deep in the US and nonexistent everywhere else. The company runs a vertically integrated exchange, clearinghouse, and brokerage structure under CFTC oversight:

That structure is why Kalshi could list a perpetual future at all. Self-clearing through Kalshi Klear plus an affiliated FCM gave the CFTC a complete regulated chain from order entry to margin custody, the framework the approval order leaned on.

Outside the United States, Kalshi holds no licenses. International members trade on the US entity under US rules, without the local investor protections a MiCA, FCA, or MAS license would carry. That gap is what Brazil, Spain, and India acted on, and it marks the structural difference between Kalshi's global posture and the locally licensed entity model OKX and Bybit adopted, covered in the OKX restricted countries guide.

Can You Access Kalshi with a VPN?

Not realistically. Mandatory KYC closes the gap a VPN would open. Identity verification ties every account to a government ID and a declared country of residence, so masking an IP at signup achieves nothing once documents are checked. Members from Restricted Jurisdictions breach the representations they make with every order, and Kalshi can restrict, suspend, or terminate membership under its Rulebook when it identifies one.

One nuance is worth knowing rather than exploiting. The restrictions key off domicile, organization, and location, and the agreement preserves Kalshi's discretion to permit platform membership from restricted regions on conditions it sets. In practice that discretion covers cases like travelers retaining account access, not onboarding UK or Canadian residents. Traders in blocked countries who want genuinely permissionless perps should look on-chain, starting with the best decentralized perpetual exchanges ranking and the Hyperliquid restricted countries breakdown.

Best Alternatives if Kalshi is Unavailable in Your Country

The right substitute depends on which half of Kalshi you wanted, the prediction market or the regulated perps. Regional picks:

- Prediction markets internationally: Polymarket serves most countries Kalshi restricts, though it faces the same wave of gambling-law blocks across Europe, Brazil, and Asia, so check local status before depositing.

- United States (perps): Kalshi itself is the new domestic option, alongside Coinbase, which won same-day approval to route US traders into international perps through an affiliate. The Coinbase Perpetuals restricted countries guide covers the details, and Kraken rounds out the CFTC-registered set per the Kraken restricted countries guide.

- United Kingdom and Canada: Event contracts are off-limits, and the FCA's retail crypto derivatives ban still applies in the UK. On-chain perps via Hyperliquid remain the most common workaround, with the caveat that it sits outside local consumer protection.

- European Union: Bybit EU (MiCA FN 636180i) and OKX Malta offer passported, regulated perps across the EEA for traders in France, Italy, Poland, and the other EU countries on Kalshi's list.

- Australia, New Zealand, Singapore: All three restrict event contracts and constrain retail crypto derivatives. Locally registered spot platforms plus the venues in the perpetual exchanges directory cover what remains accessible.

- High-leverage optional-KYC: BloFin leads the offshore optional-KYC category, detailed in the BloFin restricted countries guide, while the lowest fee crypto perpetual exchanges ranking sorts the field by cost.

Confirm the licensing position in your country before funding any account. Regulated access protects both your capital and your tax standing.

Bottom Line

Kalshi's geography runs opposite to nearly every exchange Coinperps covers. Offshore perps venues serve the world and block America. Kalshi serves America with the first CFTC-approved perpetual futures and turns away 54 jurisdictions, including most of the English-speaking world and much of Western Europe, on the event contracts side.

The 2026 story is that access is decided in two places at once. Kalshi's Member Agreement sets the official list, while gambling regulators in Brazil, Spain, and India have shown they will block the platform regardless of what that list says. International members hold accounts on a US exchange with no local license behind them, and more countries are testing that arrangement each quarter.

For US traders, the calculus is simple: regulated perps on 13 crypto assets, clearing through Kalshi's own DCO, with margin held in protected futures accounts. For everyone else, the perpetual exchanges directory and live funding rates and open interest trackers map the venues that actually serve your region.

Frequently Asked Questions

Can you trade Kalshi contracts through Robinhood or Webull?

Yes. Both brokers list event contracts that route to KalshiEX as the underlying exchange, so US users can trade Kalshi markets without opening a Kalshi account. Broker access follows the same federal framework but is US-only, so it does not create a path in for residents of restricted jurisdictions.

How are Kalshi profits taxed?

Kalshi issues US tax forms to members, and event contract gains are reportable income under US rules. International members receive no local tax reporting, since Kalshi holds no licenses outside the US, and remain responsible for declaring profits under their own country's income or capital gains rules.

What fees does Kalshi charge on event contracts?

Kalshi charges trading fees per contract using a formula tied to contract price, peaking on contracts priced near 50 cents and shrinking toward the extremes. There are no deposit fees, and the published fee schedule on kalshi.com applies identically to US and international members.

Does Kalshi pay interest on idle cash balances?

Yes. Kalshi pays yield on uninvested cash held in trading accounts, currently around 4% annually, which it can offer because member funds sit in regulated futures accounts invested under CFTC rules. The rate floats with US interest rates rather than being fixed.